This Week at MANIFEST (3/27/2020)

“Everybody who has ever invested during our darkest days has ultimately been rewarded. There’s no reason to think this time is different.” — Michael Batnick

“In the next two weeks we will witness a breathtaking degree of human ingenuity. It’s starting to bubble up now. The most capable among us are now fully engaged. That virus doesn’t know what’s coming for it.” — Scott Adams

“… for young investors, this is perhaps a once in a lifetime gift, and they should do their best to open and make maximum contributions… — Jim O’Shaughnessy, A Generational Opportunity

We’re Clearly NOT In Kansas, Anymore … Toto

The 1996 movie, Twister, features Helen Hunt, Bill Paxton, Jami Gertz and Cary Elwes, and depicts a group of storm chasers researching tornadoes during a severe outbreak in Oklahoma.

There’s a scene in the movie where the chasers dine at Aunt Meg’s house in a sort of scrambled eggs and pancakes royal feast. (And beef, it’s Oklahoma, after all…) They return to Aunt Meg’s a few hours later to find the house leveled by a tornado. Aunt Meg and her dog are rescued from the debris and the balance of the movie revolves around seeking refuge, dodging flying cows … and the ultimate final scenes where Helen Hunt and Bill Paxton strap themselves to a pipe in a barn as the entire enclosure is removed from around them. And then it’s gone … the sun comes out and clear skies manifest.

“Things go wrong. You can’t explain them, you can’t predict them. … You gotta move on. Stop living in the past, and look what you got right in front of you.” — Bill Harding (Bill Paxton)

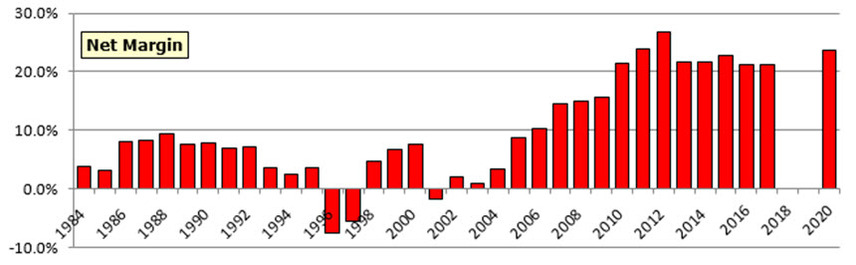

The central theme of the movie is to chase down and “inject” a tub of monitoring devices into the center of a tornado so that scientists could study anatomy, vectors, etc. and improve predictive capabilities for the benefit of many. One of these modules of sensors is shown in the accompanying figure and is named “Dorothy” in obvious tribute to those who’ve navigated over the rainbow.

But the real life, the device called “Dorothy” was actually named TOTO by the National Oceanic and Atmospheric Administration (NOAA). TOTO — which stands for “TOtable Tornado Observatory” — was a 55-gallon barrel outfitted to record storm data.

Enter our own “Dorothy” …

Whether we’re dealing with black swans, or a herd of buffalo simply trying to decide how to vector, or the wreckage from Aunt Meg’s house — clarity is a good thing. And although this won’t be perfect, at least we can come to terms with moderating forecasts as we attempt to understand how deep and how wide the current chasm challenge might be.

All 1400 companies that comprise the Value Industrials have current forecasts for 2020, 2021 and 2022 in our database. These are continuously updated (via YCharts) and will be shared frequently (at least weekly) going forward.

We’ve already seen that actual results for 2019 swooned while many people continued to marvel at “the best economy in the history of our country.” The rhinos on CNBC speak of unprecedented and undamaged “fundamentals.” They’re probably very, very wrong. My take is that it’s far from cataclysmic but not nearly as strong as many believe … and spew.

As recently as 3Q2019, expectations were for a median net margin of 8.5-9% for calendar 2019. As shown here, that didn’t happen. (Despite all of the fiscal stimulus and churning of stock buybacks, etc.) Expectations were for 9.0-9.5% in 2020. We’ll monitor very closely to see how much of a shortfall to expect, displaying it as soon as possible. But the 2020 year end median net margin went from 8.4% to 8.0% in just the last week.

[The main characters are in the shed hiding from an F5 tornado and Bill sees water pipes coming out of the floor.]

Bill: Here! These pipes go down at least thirty feet, if we anchor to them we might have a chance!

Jo: Have you lost your nerve?

Bill: Tighten your seatbelt.

Whether we’re talking about empty planes or empty restaurants… this too shall pass. We persisted through challenging times in November 2008 … backing up the truck and stepping on the gas in March 2009. We don’t have 30 feet of submerged pipe but we have nearly eight decades of wisdom and lessons deployed. We’ll chase the storm, dodge the flying cows … and attempt to navigate prudently this time, too.

- 1. Apple (AAPL)

- 21. Skyworks Solutions (SWKS)

- 25. Intel (INTC)

- Acuity Brands (AYI)

- Apple (AAPL)

- IPG Photonics (IPGP)

- NVIDIA (NVDA)

- Skyworks Solutions (SWKS)

- Universal Display (OLED)

Best Small Companies (2020 Dashboard)

The status of the 2020 Best Small Companies can be tracked at: https://www.manifestinvesting.com/dashboards/public/best-small-companies-2020

Investing Round Table Sessions (Video Archives)

- March 2019 (BKNG, SCHW)

- April 2019 (AMTD, CCMP, CPLG, SUPN)

- May 2019 (AL, SCHW, REGN)

- June 2019 (FLWS, FWRD, IIVI, PETS)

- July 2019 (ARDX, ATD.B.TO, LMNR, MKSI, MOS)

- August 2019 (ARDX, DOW, GOOG, MMSI)

- September 2019 (EPAM, FDX, ULTA)

- October 2019 (BSTC, GOOG, TXRH)

- November 2019 (BEAT, CMD, FIVE, ITRN)

- January 2020 (GILD, MIDD, MMS, SKX, VMW)

- February 2020 (ASGN, GILD, SCHW, NCLH)

Investing Topics (Video Archives)

- Turnout Tuesday: Of Tortoises & Rabbits (October 2018)

- Turnout Tuesday: Contesting Complacency (December 2018)

- Turnout Tuesday: Difference Years Make, R-E-S-P-E-C-T, Groundhogs (February 2019)

- Turnout Tuesday: The War On Our Stock Studies (April 2019)

- Turnout Tuesday: Cognizant Nation (June 2019)

- Turnout Tuesday: Time To Cook … Crystal Blue Persuasion (September 2019)

- Portfolio Management In Volatile Markets (September 2019, Portland)

- Turnout Tuesday: ROC The House! (December 2019)

- Of EAGLEs and Vigilance (December 17, 2019)

Results, Remarks & References

- Pharma Does Its Best Work Under Pressure (Morning Brew) (GILD)

- A Generational Opportunity (Jim O’Shaughnessy)

- We Will Get Through This (Morgan Housel)

- Sorry, We’re Closed (Barry Ritholtz)

- Historic Sell Off & Game of Expectations (Ben Carlson)

- Will Higher Seasonal Temps Help Versus Covid-19? (Joshua Brown)

- Evidence Over Hysteria (Aaron Ginn, Medium)

- How I’m Managing My Own Money Through This Crisis (Ben Carlson)

- Good News About The Covid-19 Pandemic (Peter Diamandis via Sigma Investment Counselors)

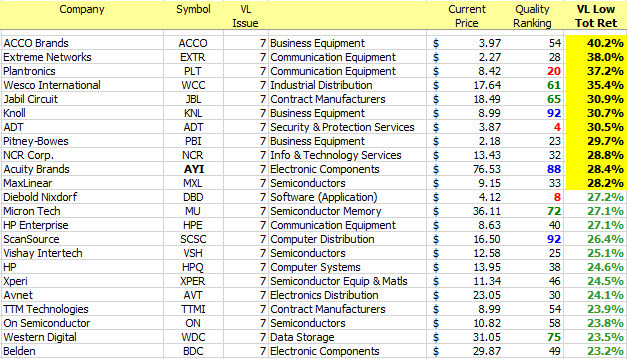

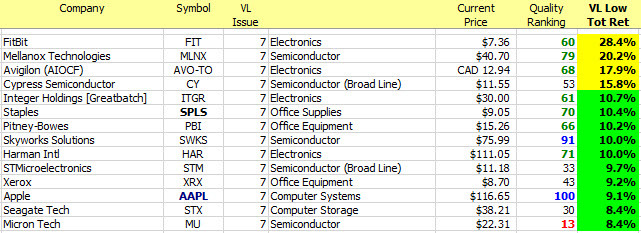

Companies of Interest: Value Line (3/27/2020)

The median Value Line low total return forecast for the companies in this week’s update batch is 14.7% vs. 18.1% for the Value Line 1700 ($VLE).

Materially Stronger: HP (HPQ), Skyworks Solutions (SWKS), Apple (AAPL)

Materially Weaker: Plantronics (PLT), Benchmark Electronics (BHE)

Discontinued: Pattern Energy (PEGI)

Market Barometers

“There’s a huge difference between an expectation and a forecast in investing. An expectation is an high-probability acknowledgment of how things might happen. A forecast is a specific prediction. In investing, forecasts are dangerous.” — Titan Research

Value Line Median Appreciation Projection (VLMAP) Forecast. The long-term median appreciation projection for the 1700 companies featured in the Value Line Investment Survey is 21.8%, INCREASING from 15.8% last week. For context, this indicator has ranged from low single digits (when stocks are generally overvalued) to approximately 25% when stocks are in the teeth of bear markets like 2008-2009.

“It is my opinion that these future appreciation forecasts are going to be revised downward (and with larger downward revisions than currently expected/anticipated) faster than someone can yell, “Fire” in a crowded movie theatre. In a word: It’s a Trap !!!” — Nick DiVirgilio

Nick is right.

Some of the geekier among us will recognize Admiral Ackbar from Star Wars:

The phrase stems from a memorable quote said by Admiral Ackbar (voiced by Erik Bauersfeld), the leader of Mon Calamari rebels, during the Battle of Endor in the 1983 Star Wars film Episode VI: Return of the Jedi. In the movie, as the Alliance mobilize its forces in a concerted effort to destroy the Death Star, Admiral Ackbar encounters an unexpected ambush, which leads him to exclaim, “It’s a trap!”

And we’re getting perhaps a little geeky, but here’s a snippet of how we’re approaching this … and why I’m optimistic that we’re barking at the right tree.

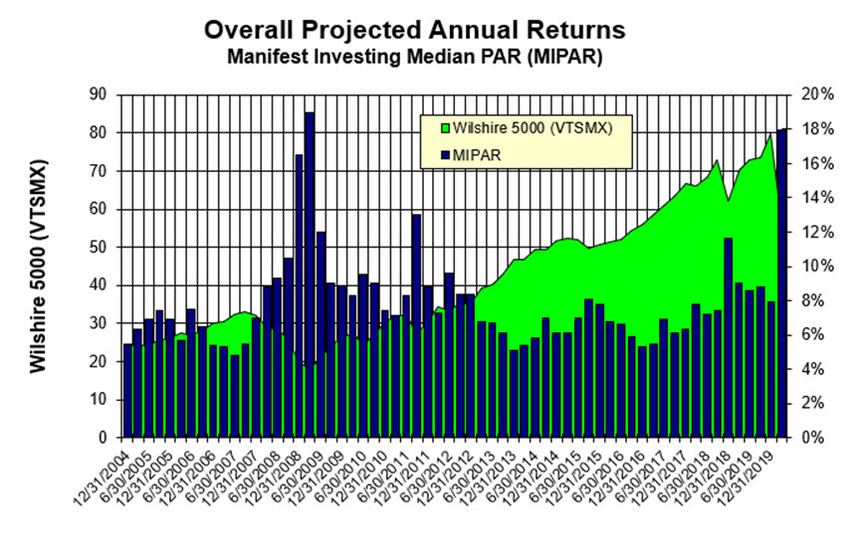

- After the stock market closed on Friday and locked in prices for the weekend, the median projected return (MIPAR) was 18.1%.

- A current data refresh of our database now displays a MIPAR of 17.4%.

- The prices didn’t change. But YCharts has been busily and dutifully updating analyst forecasts (most likely from work-from-home environments) all weekend long and this bolsters my instincts on this.

There’s no way to know the duration and amplitude of this disruption — but at least we’re not flying blind with “static analyses” on the positions that we follow.

But … chances are … we’ll have a much better perspective on the CHASM than “average investors”.

Or, as Mr. Spock would say, “it’s only logical, Captain”. — Ted Brooks

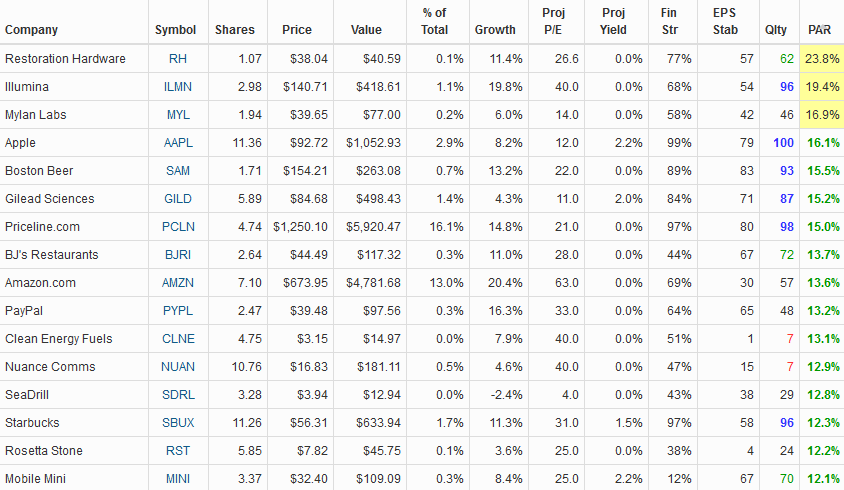

Update Batch: Stocks to Study (3/27/2020)

Long & Short Term Perspectives. (March 27, 2020) Proj Ann Return (PAR): Long term return forecast based on fundamental analysis and five year time horizon. Quality: Percentile ranking of composite that includes financial strength, earnings stability and relative growth & profitability. MANIFEST Ranking: Combination ranking that equally weights PAR and Quality. VL Low Tot Ret: Value Line forecast, expressed as low total return forecast. Owner’s PROC: Projected Return on Capital via 5-year EPS forecast versus current capital — equity and debt. Morningstar and ACE and P/FV: Price-to-Fair Value estimates from the (2) sources. 1-Yr ACE Tot Return: One year total return estimates via ACE.

Market Benchmarks (Continued)

Value Line Arithmetic Average. We’ve reached relative strength levels that suggest potentially oversold. But a reminder nudges away in that the bouncing ball bounced at a “bottom” for several months from November 2008-March 2009, a period that seemed like a very, very, long time.

Manifest Investing Median Return Forecast (MIPAR). Reaching those levels seen in 2008-2009.

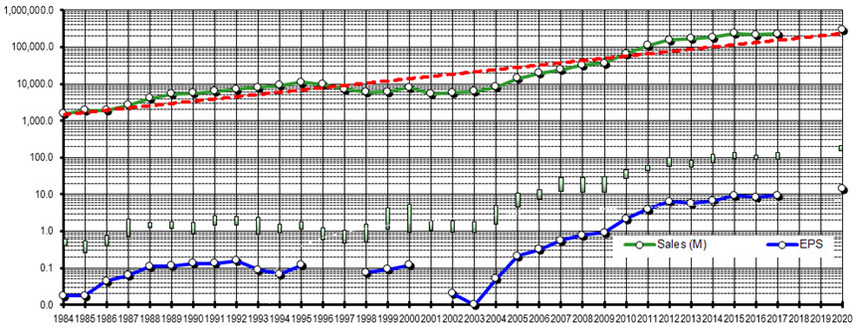

Value Line Industrials. Net Margin Not much change as the last few “precincts” for 2019 report in with their actual 4Q and 2019 year-end actuals. But we dropped from 8.4% to 8.0% on the 2020 estimates with a little erosion on the 2021-2024 expectations.

This one’s for Ted Brooks. Because he’s right about the algos and the Rise of the Machines.

You can’t look at this without noticing the daily transaction volume in the last 30 minutes or so (actually 15 … or 5) minutes of trading every day.

Surrender, Dorothy?

Whoa.

We didn’t expect our version of “Dorothy” (or TOTO) to capture the changing landscape quite this quickly.

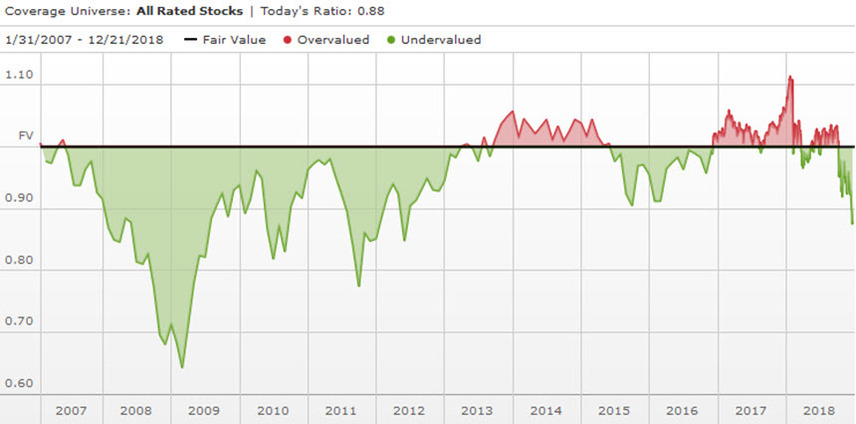

Sure. Our beloved Wall Street rhinos are back at their desks — many of them probably working from home — and they’re clearly not in a good mood. A quick comparison of this weekend’s chart shows no improvement in 2019 … with continued declines in 2020E and 2021E … and the slope of the long term trend has already deflected enough that we can “feel” it in our return forecasts.

Stock Advisor Rule Breakers. Based on the flagship Motley Fool newsletter, $100 is invested into mentioned companies. The top 16 (by

Stock Advisor Rule Breakers. Based on the flagship Motley Fool newsletter, $100 is invested into mentioned companies. The top 16 (by