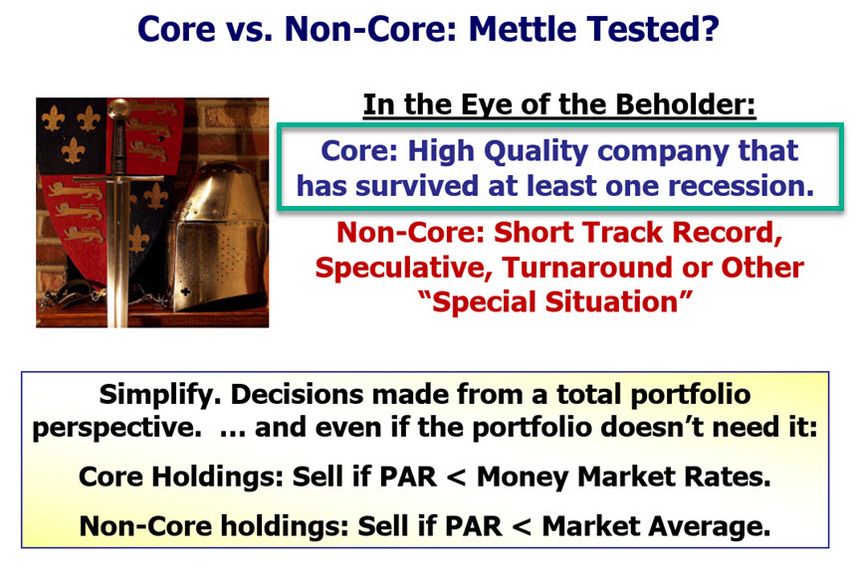

The Core/Non-Core discussion was a thought starter for sure. Clarifying my thought, adding ‘Successfully’ to ‘Survived At Least One Recession’ means to me that the company was ‘at least’ earnings profitable during a recession period. An example would be UTHR owned by the investment club I belong to. — Marty Eckerle, Cincinnati

[Here is one of the slides used in the discussion …]

Selling Decisions Based on Relative Return

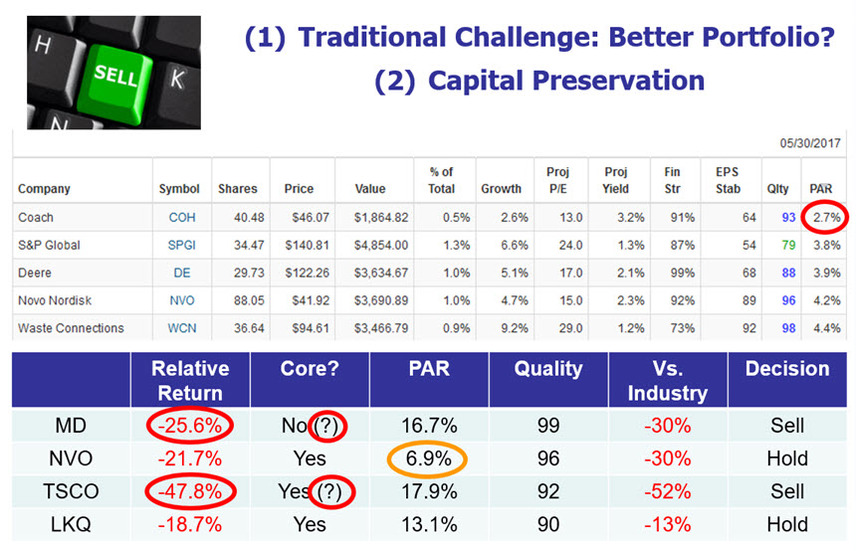

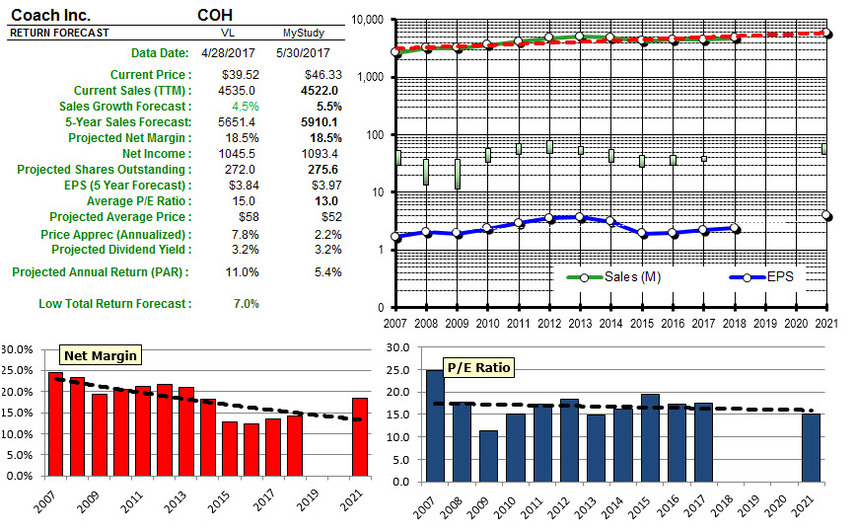

Nothing about the traditional selling decision, or Challenge, changes. We still sell with the overall portfolio characteristics in mind. It’s a standard procedure to challenge the holdings with the lowest return forecast. This was referred to by George Nicholson as “Rule One” for portfolio management. For this month’s meeting, Coach (COH) was challenged, updated, analyzed and sold to provide some boost to overall portfolio PAR.

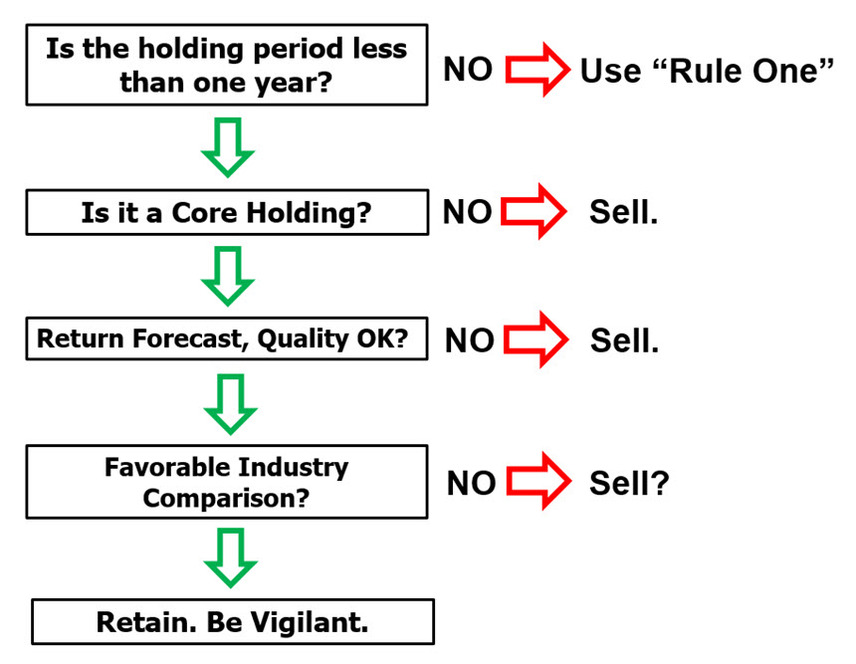

Following that, any company selected within the trailing 12 months that lags (falls behind) the Wilshire 5000 and exhibits a relative return of -20% is subjected to some “head scratching.” The following flow/decision chart is an attempt to capture this process.

Selling Decisions (May 2017)

How To Use This Chart. This chart summarizes the decisions made by checking various attributes of stocks that have triggered the -20% relative return threshold over the last year.

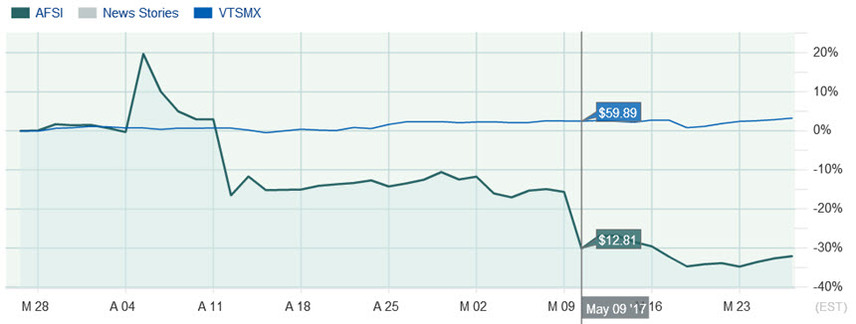

The first chart is a dashboard sorted by PAR (Ascending). The stock at the top of the sort, Coach (COH) is therefore — on the HOT SEAT. After further discussion and the update included in this thread (see below), Coach did not survive and was SOLD.

When a stock reaches a relative return of -20% (versus the Wilshire 5000, VTSMX) it qualifies for this raking over the coals. The relative performance is displayed in the Relative Return column. If LKQ (LKQ) can remain under -20%, it will be removed from this listing at future Round Tables.

Core? is a decision as to whether a stock should be subjected to tighter constraints or given “blue chip” treatment with a “longer leash.” Most participants tend to regard Retail/Apparel companies as Non-Core and we’ve found over the years that steady forecasts and steady results are generally the hallmark of companies that we consider to be core.

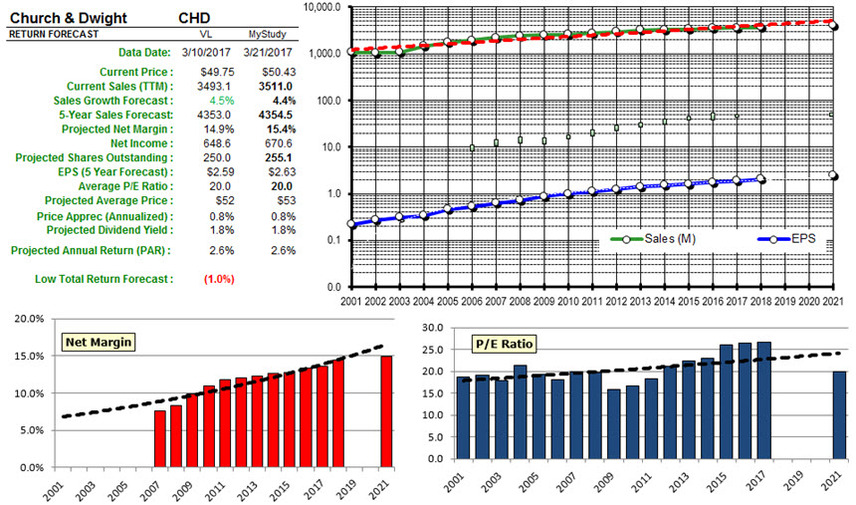

If a company is deemed to be core, a quick check of the return forecast (PAR) and Quality is in order to detect degradation or erosion of expectations. In this case NVO is definitely “on the fence” and we’re monitoring for signs of further weakness. It was noted that the stock price performance has been stronger over the last few weeks.

The last “life line” (vs. Industry) is a quick check to see if a company is actually faring relatively well versus its industry or peers while lagging the market. This essentially “saved” LKQ last month as we noted that the Auto & Commercial Vehicle Parts Index (BigCharts: WSJUSIXOTA) has lagged the overall stock market.

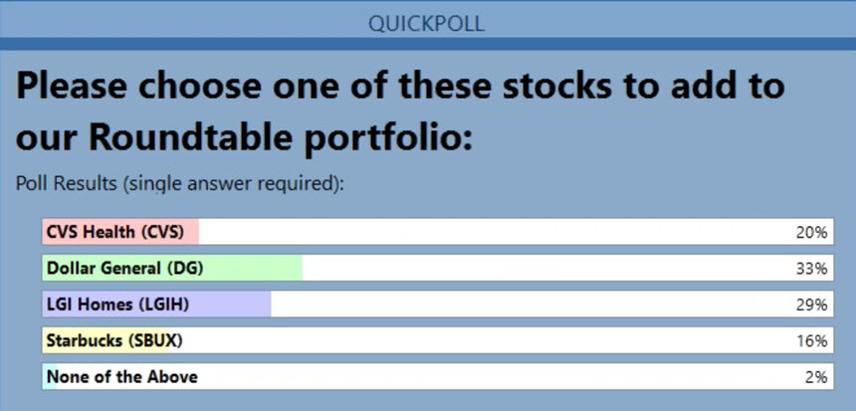

The Audience Poll was a bit of a photo finish for May 2017. We ruled that the audience selected both Dollar General (DG) and LGI Homes (LGIH) and will invest $1000 in each. The live audience in Cincinnati on 5/19/2017 selected CVS Health (CVS).