This Week at MANIFEST (12/28/2018)

“Patience is genius in disguise.” — Various, including Hugh McManus

“A 10% decline in the market is fairly common—it happens about once a year. Investors who realize this are less likely to sell in a panic, and more likely to remain invested, benefiting from the wealth building power of stocks.” — Christopher Davis

“You make most of your money in a bear market, you just don’t realize it at the time.” — Shelby Cullom Davis

“A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at good prices.” — Warren Buffett

““Is value investing dead? I don’t know. I don’t care. I don’t know when we will know. What I do know is that Warren Buffett says that growth investing and value investing are actually joined at the hip. (Tom O’Hara said this, too.) Valuation Investing is the blend of growth and value investing.” — Joel Greenblatt

Get Me Through December?

Eddy Elfenbein shared the unpleasantness update in this week’s Market Review at crossingwallstreet.com:

The numbers are remarkable. On Thursday, the S&P 500 closed at its lowest level in 15 months. In the last 12 trading sessions, the S&P 500 has lost 11.6%. The details are even uglier. Within the index, 423 stocks are now trading below their 200-day moving average. On Thursday, new lows beat new highs 175-0.

20 Years With The Value Line Arithmetic Average ($VLE). Some context. We’ve seen similar moments like this before. But there’s no denying that the December “candlestick” is in a league of its own … rare company. We’re approaching long-term “Oversold” conditions as suggested by the relative strength index (RSI) nearing 30 and relative long-term lows. We’re reminded that the trailing 52-week returns have dipped sub-zero a few times in the last few years — so this should not be regarded as something new or unusual.

Manifest Investing Median Return Forecast (MIPAR). It’s clear that the median (basically average) return forecast for the 2300-2400 companies in our coverage universe have SUDDENLY shifted to new levels due to the price drop. This could also happen from a breach of fundamentals — but that is NOT the case, here … at least not yet. Return forecasts are now at levels we haven’t seen since 2008-2009.

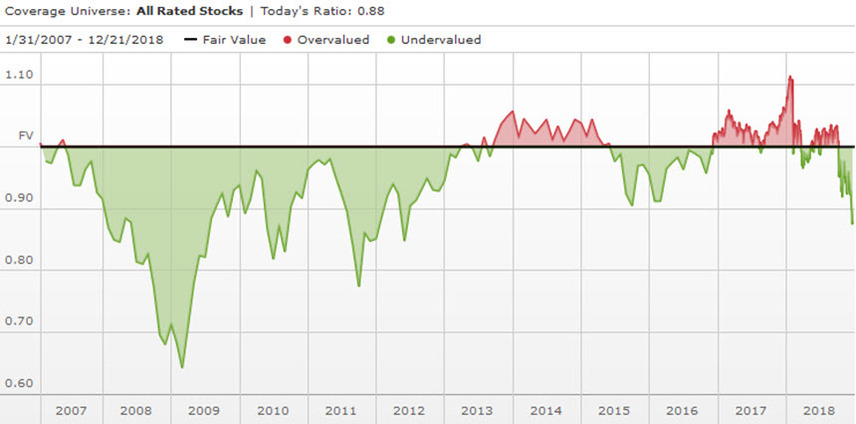

Source: https://www.morningstar.com/tools/market-fair-value-graph.html

Beyond December — A Hope For Fewer Potholes …

My take on all of this carnage? It’s different this time.

Yes, I said the words.

Bear markets and corrections are pretty unique despite all of our attempts to slap historical price chart overlays and compare factors, etc. The simple truth is that (1) the sample size will never be statistically sufficient for any material conclusions to be reached. [Yet the Rhinos will continue to try. Smile and nod at them.] (2) Markets are not rational.

Current conditions definitely qualify for a sedative or something stronger.

Look no further than the accompanying weekly chart of the Value Line Low Total Return Forecast to see how sudden the current price correction has been. We’ve not seen a change with this velocity or ferocity since 2008. You remember, right? With Christmas carols humming in the background, recall the names Bear Stearns, Lehman, Merrill Lynch and things like credit default swaps and neighbor’s houses in foreclosure.

Yes, there’s a mountain of uncertainty and an abyss of incivility inside the Beltway and a President who’s certainly disruptive. But the core problem with the status is virtually unchanged — ALL of the political posers persist in patching or ignoring potholes (healthcare, immigration, infrastructure, federal capital structure, failed nation building, sloped international trade playing fields, the ostriches and lobbyists related to real capital markets reform, etc.). The hypocrisy is gut wrenchingly prevalent.

I think the stock market is legitimately tired of the perpetual motion of Congressional Kick The Can Down The Road — and corporations are suddenly much more guarded about faith in consistency and less optimistic that the moving targets have abated. As the foot comes off the accelerator and taps the brakes (again) we might return to the recessionary conditions of 2015-2016. Much of the globe is already headed there.

Unattended potholes become sinkholes.

Like snowflakes, it’s different this time. It’s always different. Trying to allocate assets or imagine outcomes based on historical models (even when powered by artificial intelligence) is a neural niblick.

So we turn to a constant. A constant that survived and thrived through the 1970s, 1987, 1994, Y2K and the gasping throes of 2008-2009. That constant is to eschew the chaos. Focus on what matters. Simply put, INVEST BETTER.

We accept that markets are not rational. We refuse to be surprised when they convulse.

We take the words of Warren Buffett quite seriously when he longs for corrective opportunities “a few more times during his investing lifetime” and speaks unflinchingly of tracking excellent companies and waiting for them to be available at attractive prices.

I believe one of those moments may have arrived. We don’t often make “market calls” but we did write about back-up-the-truck moments back in November 2008 (a wee bit early) and March 2009 (squarely in the bullseye). This could be another Buffett Bonanza.

So … we think it’s prudent to do what we’ve done for DECADES. Discover excellent companies, BETTER COMPANIES. Buy those that are priced well. BETTER PRICES FOR BETTER RETURNS.

Hugh McManus likes patience and its genius-making potential. He also likes excellent companies trading near their 52-week or multi-year lows. We’re thinking Hugh must be beside his Irish self these days and hope to hear from him during next weekend’s Round Table. Ken Kavula is sure to be swimming in the pool of sudden small company opportunity. Cy Lynch is likely to admire the latest bear market which will become a future blip. Rest assured that we’ll be more focused on the long term perspective than any pusillanimous politicians and their potholes, meandering Rhinos or any of those annoying talking heads who focus on “how much your 401(k) LOST since breakfast today.”

We promise to remain focused on the discovery and sharing of the best ideas — the opportunities we’ve known for decades as BETTER COMPANIES at BETTER PRICES.

Merry Christmas to our favorite nation of focused and compassionate investors!

Best Small Companies (2019 Dashboard)

The status of the 2019 Best Small Companies can be tracked at: https://www.manifestinvesting.com/dashboards/public/best-small-2019

- 1. Apple (AAPL)

- 23. Skyworks Solutions (SWKS)

- 26. Intel (INTC)

- Apple (AAPL)

- IPG Photonics (IPGP)

- MKS Instruments (MKSI)

- Skyworks Solutions (SWKS)

- Universal Display (OLED)

Round Table Sessions (Video Archives)

- January 2018 (ADS, SBUX, SWKS)

- February 2018 (CWH, HCSG, MCK, PBH, SIRI)

- March 2018 (AYI, GE, MCK, WAL)

- April 2018 (GE, SBUX, ULTA)

- May 2018 (ALRM, ADS, CBRE, CTSH, FIVE)

- June 2018 (BECN, BMY, OLED)

- July 2018 (CTSH, COHR, IONS, SKX)

- August 2018 (IPGP, LCII, WH)

- September 2018 (LCII, SLP)

- October 2018 (ARDX, LMAT, MKSI, UNFI)

- November 2018 (FB, FLT, IIVI)

Turnout Tuesday Educational Sessions

- Turnout Tuesday: Investing In Overheated Markets (February 2018)

- Turnout Tuesday: Taxes & Impact on Stock Studies (April 2018)

- Turnout Tuesday: Quality Trends & Selling (June 2018)

- Turnout Tuesday: What’s It All About, Alpha? (August 2018)

- Turnout Tuesday: Of Tortoises & Rabbits (October 2018)

- Turnout Tuesday: Contesting Complacency (December 2018)

Results, Remarks & References

- Why We Sold Apple Stock (Vitaliy Katsenelson)

- Index Investing Critic Takes Aim. Fires. Misses. (Barry Ritholtz)

- Masters In Business: Jeremy Grantham (Barry Ritholtz)

- An Evolve Or Die Moment For The World’s Great Investors (Fortune via Kim Butcher)

- Crossing Wall Street Market Review — 12/21/2018 (Eddy Elfenbein)

- Buying When Stocks Are Down Big (Ben Carlson)

Companies of Interest: Value Line (12/28/2018)

The median Value Line low total return forecast for the companies in this week’s update batch is 12.3% vs. 10.8% for the Value Line 1700 ($VLE).

Materially Stronger: Vishay Intertechnology (VSH), Office Depot (ODP), Kemet (KEM)

Materially Weaker: TTM Technologies (TTMI), Diebold Nixdorf (DBD), Western Digital (WDC), Plantronics (PLT), STMicroelectronics (STM), Micron Technology (MU), Cirrus Logic (CRUS), Lattice Semiconductor (LSCC), Celestica (CLS), 3D Systems (DDD)

Discontinued: Spectra Energy Partners (SEP)

Market Barometers

The thing very few people tell you about “overvalued” markets is that, occasionally, the fundamentals arrive to justify them. — Joshua Brown

Value Line Low Total Return (VLLTR) Forecast. The long-term low total return forecast for the 1700 companies featured in the Value Line Investment Survey is 10.8%, increasing from 8.5% last week. For context, this indicator has ranged from low single digits (when stocks are generally overvalued) to approximately 20% when stocks are in the teeth of bear markets like 2008-2009.