This Week at MANIFEST (4/24/2015)

One of the Best Long-Term Forecasting Methods

“If you have to forecast, forecast often.” — Edgar R. Fiedler in The Three Rs of Economic Forecasting-Irrational, Irrelevant and Irreverent , June 1977.

It was two years ago that Mark Hulbert featured some words about our approach to long-term forecasting in the context of some editorial on the efficacy of The Value Line Investment Survey.

We have noted — over the years — that actual returns tend to more closely resemble the low return forecasts on the company research pages for Value Line. Since 2001, the average Value Line low total return forecast has been 7.9%. The actual returns over that time frame have been 6.5%.

Here’s a quarter-by-quarter illustration of forecast vs. actual for the Value Line companies:

This was essentially what Mark Hulbert was sharing in the article, Finding The Best Four Year Market Forecaster.

To us, although the absolute math is important — what really matters is the “shape.” This would suggest that we’ve still got a few quarters of upward-sloped plateau ahead of us. But the “swoon vulnerability” is still pretty high and the reality is that no one knows when the next market break will hit or how “corrective” it will prove to be.

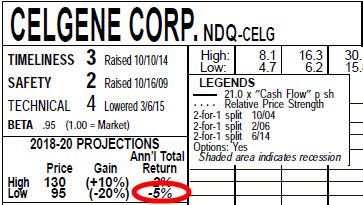

Companies of Interest: Value Line

The average Value Line low total return forecast for the companies in this week’s update batch is 3.0% — lower than the 3.7% for the Value Line 1700.

Less turbulence again this week in the updates although there were more companies dropped from coverage than we’ve seen in a very long time.

Materially Stronger: GEO Group (GEO), Daktronics (DAKT)

Materially Weaker: DeVry (DV), Philip Morris International (PM), Career Education (CECO), Zynga (ZNGA), Boulder Brands (BDBD)

Standard Coverage Initiated:

Discontinued: Safeway (SWY), Pantry (PTRY), Silicon Image (SIMG), Chiquita Brands (CQB), LeapFrog (LF)

Market Barometer

Value Line Low Total Return (VLLTR) Forecast. The long-term low total return forecast for the 1700 companies featured in the Value Line Investment Survey is 3.7%, a slight decrease from 3.8% last week. For context, this indicator has ranged from low single digits (when stocks are generally overvalued) to approximately 20% when stocks are in the teeth of bear markets like 2008-2009.

For more on this chart: Origins of the $USHL Indicator

Stocks to Study (4/24/2015)

- Synchronoss Tech (SNCR) — Highest MANIFEST Rank

- Daktronics (DAKT) — Highest Low Return Forecast (VL)

- ROVI (ROVI) — Lowest P/FV (Morningstar)

- Fresh Market (TFM) — Lowest P/FV (S&P)

- Rosetta Stone (RST) — Best 1-Yr Outlook (ACE)

- Tyson Foods (TSN) — Best 1-Yr Outlook (S&P)

- Keurig Green Mountain (GMCR) — Best 1-Yr Outlook (GS)

I’ve been giving some thought to a database-wide screening summary of “deeper value” opportunities that we’d publish on Tuesdays. Keep in mind that the results of our Monday morning efforts are focused — as they should be — on 1/13th of the stocks we cover and on behalf of shareholders and stock watchers.

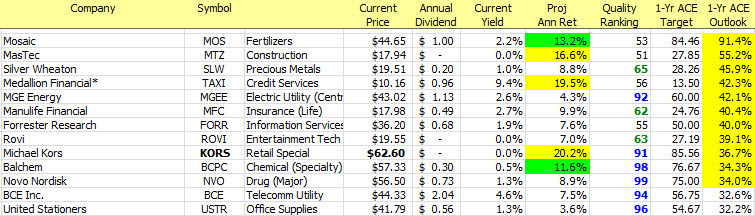

Proposing a “Dirty Dozen”

OK, it’s really a Baker’s Dozen — culled from the full database and it’s based on two things:

- Better Than Average Quality

- Highest Analyst Consensus Estimate-based (ACE) Expectations for the year ahead

I’m thinking that it could be meaningful when these opportunities converge with the longer term opportunities. The table provides the top (13) such companies on 4/21/2015 — and we’ll see how this behaves/performs over the next few months.