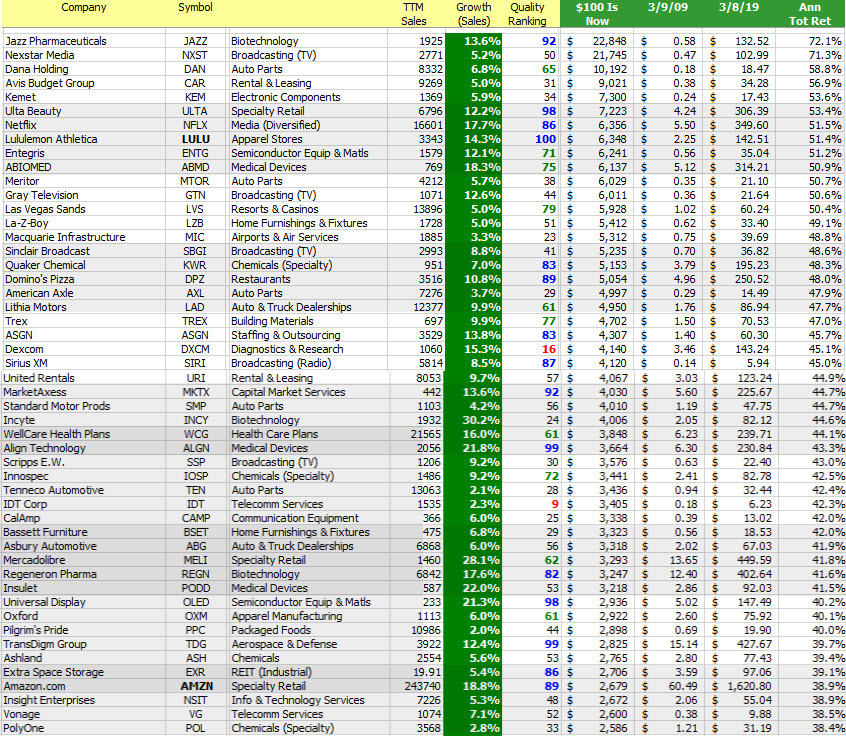

After a cursory review, I’m wondering if this book doesn’t have the potential to parallel (and rhyme with) Nicholson’s 1984 Individual Investor’s Manual and for that reason, I’ve ordered my advance copy for a closer look. As you read this overview, notice how often the things he says, starting with the definition of risk through the eyes of a disciplined long-term investor, the recovery following the Great Recession of portfolios like Tin Cup … and a host of other philosophies that we hold dear, including but not limited to our practice of all-of-the-above investing. (Note his references to the equally-weighted Wilshire 5000) His objective mapping even resembles our +5% mantra. I look forward to a closer look and sharing thoughts with our community of investors during a future book review.

Looking at Investment Risk the Wrong Way

by James B. Cloonan, AAII Founder and Chairman

We have all been looking at investment risk the wrong way. And unfortunately we have been paying dearly for this mistake. Please allow me a moment to explain this statement and to teach you how you can change your day-to-day investment approach to compensate for what has more than likely been years of under performance.

You can easily produce much more investment return if you are willing to embrace what I call Level3 logic and reason when dealing with your investment program. The simple truth is that every long-term investor will hit two, perhaps three, major market downturns in their investment life.

Historically, these major downturns take only 3 to 4 years to recover from (come back to even) if you were to do nothing but simply stay in the market. Remember, markets have historically always risen and that is a great advantage for the individual investor … But the financial press, CNBC and Wall Street has everyone brainwashed to believe that we need to put 40%, 50% or even 60% of our assets into so-called safe investments (bonds and cash). Investing with that level of safety is insane when you realize that since 1871 market downturns have recovered as follows:

- 33% of market downturns recover within a month

- 50% of market downturns recover within 2 months

- 80% of market downturns recover within 1 year

- 95% of the time, those big “once or twice in a lifetime drops” return back to even in 3 to 4 years with an appropriate portfolio

Collectively, since 1871 the time it takes for the market to recover (top to trough to top again) is a mere 7.9 months. (This context and perspective is urgent to understanding what we do and how we do it.)

Unfortunately, most individual investors watch daily, weekly, monthly and quarterly market moves like their life depends on it. The logical and far more reasonable way to invest is to put only what you will need to withdraw from your portfolio for living expenses over the short term into extremely safe (cash-like) accounts and to invest the rest of your assets in stocks. I define short-term as 3 to 4 years. This is a logical and rational use of funds that serve as a safety net that can be used to ride out any downfall Mr. Market throws our way. It also serves to keep us from having to focus on the near-term performance results of our portfolios. Having a near-term safety net allows investors to be more aggressive in the overall stock portion of their portfolios while being able to simultaneously ignore short-term market swings.

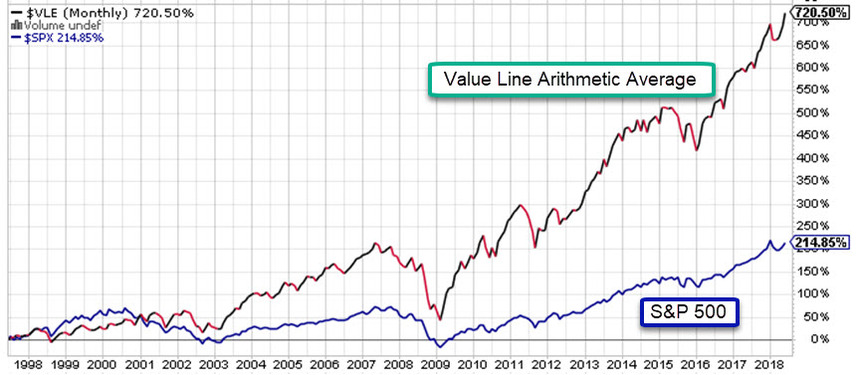

The equal-weighted Wilshire 500 index represents a much broader basket of companies and has a much larger number of small-cap and mid-cap stocks in its holdings. That smaller company skew is what propelled the Wilshire 5000 equal-weighted index up to an annualized return of 17.1% over the past 45 years (the longest data set available for this segment of the market).

Trust me when I say that long term most investors would be jumping up with joy to achieve just the S&P 500’s return. But the fact is, most investors fail to come even close to the overall market return, let alone our favored cousin – the equal-weighted Wilshire 5000. In-the-know researchers and studies from actual brokerage account transactions show that most investors get into and out of the market at the absolute wrong time. That coupled with their fixation on large-cap growth stocks has produced returns that are closer to 7% or 8% on an annualized basis.

Following the Level3 Investing approach that I have developed allows investors the ability to implement 3 investor advantages that can propel portfolio returns and generate huge sums of wealth:

Advantage #1—My Level3 Investment Strategy teaches you how to understand and use risk to your advantage by building a cash cushion that will weather any market downturn. Simultaneously the strategy frees you to put more of your assets into higher returning portions of the investment marketplace – individual stocks and a handful of passive ETFs (I call them forever funds.)

Advantage #2—Level3 Investment Research has tapped into academic and time-tested studies to show beyond a reasonable doubt that investment portfolio growth comes from small and mid-cap stocks not large-cap companies. So if you are a long-term investor, you should be looking closely at building up not only the overall size of your equity portfolio but the percent you equate to small and mid-cap stocks and funds. Remember, these are the types of investments that history shows have outpaced the overall market by more than 4% per year. Average investors produce 8% return, while a Level3 approach should produce 12%. Regardless of the size of your portfolio, that 4% difference will provide you with twice the assets of a regular investor in 18 short years.

Advantage #3—Level3 Investing drives home the use of Time Diversification. My new Level3 approach uses investment research that has proven that no matter how much the equity market collapses it historically has always exceed its previous high.We know that investing can be difficult when markets drop, but as an individual investor you must remember that history shows that all dips all crashes and all drops ultimately lead to higher returns. Market data since 1871 bears this out. And best of all, the kinds of stocks that Level3 investing favors are the kinds of stocks that rebound the fastest! Going forward, if you can keep the concept that time favors the individual investor in the forefront of your mind, you will find that investing becomes much easier.

If you are interested in becoming a Level3 type of investor, I encourage you to do the following …

Accept that true investment risk is not some arbitrary percentage downfall in the market this day, week, month or year, but that investment risk is actually failing to meet your retirement lifestyle goals because the funds we reasonably expect to have are NOT THERE when needed. That’s the Level3 definition of long-term risk, not having the assets needed to live the life you deserve!

Think about what it means to be a true long-term investor and recognize that any funds you need in the next 4 to 5 years should simply not be invested in stocks or bonds. Your near-term spending needs should be placed in money market accounts, CDs or savings. Thus when and if the market drops, near-term you know that you will have the funds needed to live your current lifestyle and not have to worry about selling at a bottom to get cash or fleeing the overall market because you are afraid of losses. This one simple strategy allows you to earmark the bulk of your overall assets into long-term Level3-type stock and fund investments that can generate wealth quicker than any other asset class.

Recognize that greater long-term [appreciation] comes from investing in smaller and mid-cap companies. If these types of holdings are not in your portfolio, consider adding them. You can start by looking into Guggenheim’s RSP or you can use the link below to purchase my new “Investing at Level3” book where I share a handful of ETFs that you could simply hold forever.

“Investing at Level3” is a refreshingly simple and historically proven way to invest that has the power to greatly impact your wealth as well as your retirement lifestyle.

The “Investing at Level3” approach, if followed diligently, could double or triple the value of a portfolio at retirement for the long-term investor when compared to today’s current investment practices. The book provides a research-driven yet easy-to-use approach to help individual investors with overcoming their unease with investment risk, investing while in retirement, investment selection, asset allocation, retirement funding and more.

Fondly,

James B. Cloonan

AAII Founder and Chairman

- The Wilshire 5000 Equal Weighted index is not generally quoted and has no symbol. There is no fund replicating it because many of the stocks have limited float, but it does serve as a good proxy for the type of investing I outline in my new book “Investing at Level3.” If I have piqued your interest, current and past values can be found at Wilshire.com under the Wilshire Index Calculator. (This is why we use the Value Line Arithmetic Average, $VLE via www.stockcharts.com)