This Week at MANIFEST (1/24/2020)

“Life is like a snowball, all you need is wet snow and a really long hill.” — Warren Buffett

This past week, we lost a very special charter subscriber to Manifest Investing. My Father. I think his ID number was single digits. He was also a charter member of our Chicago-based investment club, evolved into an investing warrior … and was quite simply, my favorite EAGLE.

A couple of weeks ago I huddled with my father over his monthly ritual of opening his E*Trade envelope. A careful slice of the envelope (he saved every single one of them, every one) and I heard him say some of my favorite words, “My Colgate-Palmolive stock is worth how much? That can’t be right.” A $2000 investment in CL was now worth $28,000. This was typical of many holdings. In fact, the gains in Gentex, Pepsi, and Vanguard Technology (VGT) were actually much bigger.

His experience with General Electric was “different.” He shared his disappointment with GE often.

But he fixated on the steady delivery of Colgate. As the accompanying image shows, the company occupied Mom and Dad’s Christmas tree. We first talked about this long ago, see: When Monsters Are Created. It’s a story about consumer and stakeholder loyalty. This past weekend, I noticed that all of the squeezed toothpaste tubes on the bathroom sinks (including those toted by his grandchildren) were Colgate. He left a mark.

The image of Mom and Dad was captured at an Investor Fair in Springfield, Illinois. Long story short, the Biomet investor relations representative had told Mom and Dad over breakfast that $2000 invested in Biomet circa 1980 was worth $1,000,000 in the late 1990s. It’s a fact. (For more, see Raise A Cup: Million Dollar Moment — April 2012) It’s also potential freedom. Magic and miracles happen when given a chance.

Dad was a magnificently complicated man. He often chided me for complaining about bears and investing. “Not all bears are bad. I give one to your mother every Valentine’s Day. Besides, we loaded up on some pretty good stocks in March 2009 thanks to one of your bears.” Much wisdom.

And, in closing, one of the simplest and 100% effective lessons ever: Lessons From Fathers & Simple Things, Solid Results (Some might note that this may have been the earliest reference to Five Below)

Bottom Line: Dad took his investment club experience back in the 1990s and deployed it with an IRA that was invested in a CD that also happened to be charging $75/year for “custodial service.” We recently calculated that it would have worth approximately $20,000 if left in that paltry “risk free” situation. We moved it to E*Trade and he carefully selected companies like Gentex, Johnson & Johnson, AFLAC, Walgreen/CVS and leaned heavily on Vanguard Technology (VGT) despite his age. His balance grew to be a lot more than $20,000. When we talked about “risk”, I observed that “Dad, you’ve NEVER, EVER, acted your age.” He didn’t think long term investing included the risk they talk about on television and teach in colleges and business schools. He was right.

For so many of the deepest lessons and love imaginable, THANK YOU, DAD.

- 23. Pepsi (PEP)

- 32. Tapestry (TPR)

- 39. Ulta Beauty (ULTA)

- 40. Costco Wholesale (COST)

- Costco Wholesale (COST)

- Dollar General (DG)

- Five Below (FIVE)

- Schwab, Charles (SCHW)

- Skechers (SKX)

- TJX Companies (TJX)

- Tyson Foods (TSN)

- Ulta Beauty (ULTA)

Best Small Companies (2020 Dashboard)

The status of the 2020 Best Small Companies can be tracked at: https://www.manifestinvesting.com/dashboards/public/best-small-companies-2020

Investing Round Table Sessions (Video Archives)

- January 2019 (ARDX, EPAM, HIIQ, TJX)

- February 2019 (ALGN, ARDX, CVS, TOT)

- March 2019 (BKNG, SCHW)

- April 2019 (AMTD, CCMP, CPLG, SUPN)

- May 2019 (AL, SCHW, REGN)

- June 2019 (FLWS, FWRD, IIVI, PETS)

- July 2019 (ARDX, ATD.B.TO, LMNR, MKSI, MOS)

- August 2019 (ARDX, DOW, GOOG, MMSI)

- September 2019 (EPAM, FDX, ULTA)

- October 2019 (BSTC, GOOG, TXRH)

- November 2019 (BEAT, CMD, FIVE, ITRN)

Investing Topics (Video Archives)

- Turnout Tuesday: Of Tortoises & Rabbits (October 2018)

- Turnout Tuesday: Contesting Complacency (December 2018)

- Turnout Tuesday: Difference Years Make, R-E-S-P-E-C-T, Groundhogs (February 2019)

- Turnout Tuesday: The War On Our Stock Studies (April 2019)

- Turnout Tuesday: Cognizant Nation (June 2019)

- Turnout Tuesday: Time To Cook … Crystal Blue Persuasion (September 2019)

- Portfolio Management In Volatile Markets (September 2019, Portland)

- Turnout Tuesday: ROC The House! (December 2019)

- Of EAGLEs and Vigilance (December 17, 2019)

Results, Remarks & References

- The Decade In Technology (Morning Brew)

- Peter Lynch: The Barry Sanders of Investing

- Of Chocolate And Lemonade (Mark Robertson)

- Elegance and Simplicity (Ken Kavula)

- Most Disruptive Trend of the Decade (Josh Brown)

- Decade in Review (Ben Carlson)

Companies of Interest: Value Line (1/24/2020)

The median Value Line low total return forecast for the companies in this week’s update batch is 5.5% vs. 4.6% for the Value Line 1700 ($VLE).

Materially Stronger: Wal-Mart (WMT), Aaron’s (AAN), Costco Wholesale (COST), AutoZone (AZO)

Materially Weaker: Conn’s (CONN), Designer Brands (DBI), Children’s Place (PLCE), Fossil (FOSL), Kohl’s (KSS), Ollie’s Bargain (OLLI), Molson Coors (TAP)

Discontinued: Avon Products (AVP), Medicines Co. (MDCO)

Note:

Market Barometers

The thing very few people tell you about “overvalued” markets is that, occasionally, the fundamentals arrive to justify them. — Joshua Brown

Value Line Median Appreciation Projection (VLMAP) Forecast. The long-term median appreciation projection for the 1700 companies featured in the Value Line Investment Survey is 8.8%, a DECREASE from 9.7% last week. For context, this indicator has ranged from low single digits (when stocks are generally overvalued) to approximately 25% when stocks are in the teeth of bear markets like 2008-2009.

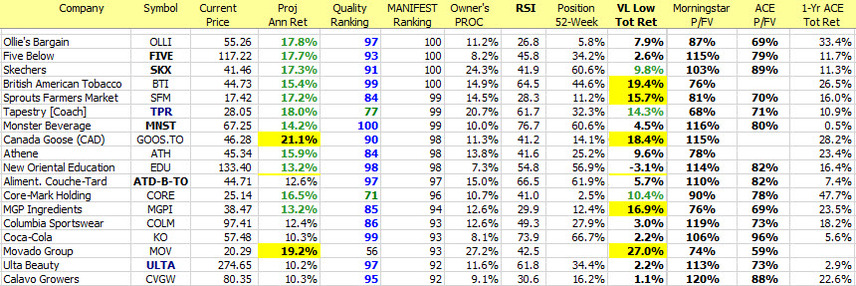

Update Batch: Stocks to Study (1/24/2020)

Long & Short Term Perspectives. (January 24, 2020) Proj Ann Return (PAR): Long term return forecast based on fundamental analysis and five year time horizon. Quality: Percentile ranking of composite that includes financial strength, earnings stability and relative growth & profitability. MANIFEST Ranking: Combination ranking that equally weights PAR and Quality. VL Low Tot Ret: Value Line forecast, expressed as low total return forecast. Owner’s PROC: Projected Return on Capital via 5-year EPS forecast versus current capital — equity and debt. Morningstar and ACE and P/FV: Price-to-Fair Value estimates from the (2) sources. 1-Yr ACE Tot Return: One year total return estimates via ACE.