Diligence. This week’s update provides an up-close-and-personal look at our weekly process for seeking actionable investing opportunities to study. Our subscribers benefit from this information starting every Monday morning with the roll call, the fundamental updates and the targeted opportunities for further study. For more on Manifest Investing, go here.

“Diligence is the Mother of good luck.” — Benjamin Franklin

“The expectations of life depend upon diligence; the mechanic that would perfect his work must first sharpen his tools” — Confucius

This week we take a closer look at our weekly report — and specifically — how we think this information is best used by long-term investors.

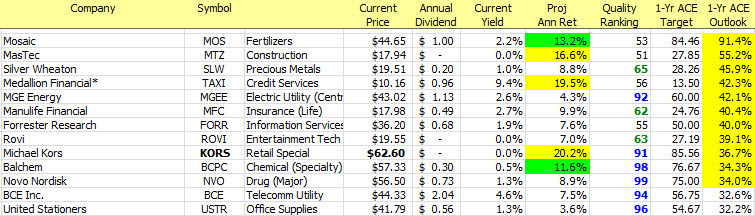

In a nutshell, we’re checking in on a few key areas. If you’re a shareholder or stockwatcher, we provide a synopsis of the best opportunities in the current (this week’s) update batch from Value Line. We update 1/13th of all companies every week and the best return forecasts for the week are on display in the Companies of Interest: Value Line section.

In the case of Tidewater (TDW), the Value Line low total return forecast (annualized for the next 3-5 years) is 25%.

This was based on the stock price shown ($25.57) on the date of analysis (4/28/2015).

The price is now $29.25 — part of the explanation for the 19.5% on our weekly report. The other source of a difference is that we’re constantly (every day) adjusting the time horizon in addition to the price. That $60 long term low price forecast is a fixed date. In any event, every Monday morning brings a roll call of best opportunities according to Value Line.

Why the Value Line Low Total Return (VLLTR) forecast? Because our research has found this to be the most reliable (actual results vs. forecasts) for the collective of companies covered by Value Line.

And about that $60 entry. This is where we flag opportunities and threats. Any material change (~20-25%) in this long term low price forecast (up or down) is flagged as Materially Stronger (up) or Materially Weaker (down) as we do our Monday morning roll call. If you’re a shareholder or stock watcher for a company that shows up in either roll call, consider it a nudge to see why Value Line seems to have adjusted their expectations — UP or DOWN.

We’ve begun to include direct links to snapshots or thumbnails for some of the flagged companies during these weekly updates. This week, we’ve started with Transocean (RIG) and recent Round Table selection Dril-Quip (DRQ).

When You’re Sailing … Do You Really Care About The Wind?

I think the answer is yes, but it depends. It depends on WHO you are and things like risk tolerance, life expectancy time horizons, opportunistic return maximizing, etc.

For a capital preservationist, we’d like to avoid turbulence like we saw during the Great Recession. This is the reason we track primary market barometers like the overall average return forecast. This characteristic doesn’t tell us when corrections, recessions or bear markets will happen — but it does help to gauge “vulnerability.” Higher quality stocks with higher return forecasts are more recession resistant. Period. On the opposite end, following a recession and significant correction, we “dial up” our interest in more speculative opportunities and increase our dosage of emerging, faster-growing companies.

Our barometers on parade are intended to give a few perspectives on “vulnerability.” The $USHL indicator that we display occasionally is a very broad — and seemingly fairly reliable indicator of rhino behavior. This was inspired by The Big Picture and Barry Ritholtz. You can dig a little deeper on this one at An Attempt to Identify Market Tops ($USHL).

Most of us do very, very little asset allocation — and frankly, it ain’t easy and it’s what most of the investors and asset managers foul up, contributing to overall negative relative returns on average for the average rhino.

That said, Nicholson counseled that when it gets extremely challenging to find stocks to buy or accumulate, it is acceptable (and potentially incrementally rewarding) to build a war chest of cash equivalents to go shopping after the recession and stock price correction has blasted stocks back to elevated return forecasts.

Our Consensus Perspective

While the Monday morning roll call is limited to the Value Line update batch and our efforts to flag threats and opportunities, we reach out and check forecasts and judgments at places like Morningstar, Standard & Poor’s, Analyst Consensus Estimates (finance.yahoo.com) and Goldman Sachs. We audit and update these various resources to generate the Stocks to Study. This list is always sorted by MANIFEST Rank, our combination ranking of return forecast and quality … and we generally limit the field to the top decile or top 5 percentiles of the stocks in the 1/13th update batch.

Polaris Industries (PII) provides this week’s example of deeper digging in the snow … and beyond the snowmobiles for the company. Did you know that snowmobiles account for less than 10% of annual revenues?