Fave Five (3/14/2017)

Our Fave Five essentially represents a listing of stocks with favorable short term total return forecasts (1 year, according to Analyst Consensus Estimates, or ACE) combined with strong long-term return forecasts and good/excellent quality rankings. The average 1-year ACE total return forecast is 7.1%.

The Fave Five This Week

- Boston Beer (SAM)

- Exxon Mobil (XOM)

- LKQ Corp (LKQ)

- Perrigo (PRGO)

- Target (TGT)

Gone Shopping With Walter (Schloss) and Hugh

“When buying a stock, I find it helpful to buy near the low of the past few years. A stock may go as high as 125 and then decline to 60 and you think it attractive. 3 years before the stock sold at 20 which shows that there is some vulnerability in it.” — Walter Schloss

“…the analyst interested in value is likely to place only minor emphasis upon the short term earnings outlook; whereas the analyst who endeavors to anticipate the price movements of the near future will make such outlook his major concern.” —

Ben Graham, Security Analysis

Hugh McManus has been a regular — and very successful stock selector — as a participant in our monthly Round Table series over the last eight years or so. Even in the months when he’s globe trotting and unable to join us, we’ll generally take a quick look for opportunities with a quick stock screen for high quality companies priced near their 52-week (or multi-year) lows. For more on this subject, see: Gone Fishing — Patiently and Disciplined Fishing

If a company is primed for long-term growth, buying it when the price is depressed is better than buying it when it’s at a 52-week high. If the stock price drops to a new low, there’s always bad news to explain the fall, which is one of those obvious truths. I had to learn whether I wanted to fixate on the bad news or focus on the low price of a good company. Most people seem to be transfixed by the news. I take it one step further and hope the bad news persists for a while — it’s where the psychiatrist would step in — as it allows me to buy more.

In 1997, or thereabouts, Ken “Mr. NAIC” Janke, commented that members of the organization were masterful at identifying quality companies, but not nearly as good at picking a low price. I had already adopted the practice of buying companies when they reached or were close to a 52-week low. It’s a rule not a law: for an idealized growth company, today’s close is the new 52-week low.

Ken Janke often spoke of the reality between the high and low prices during a given year for virtually all companies. The range is bigger than most people realize, as underscored by the accompanying chart via Saber Capital Management and John Huber.

Patience is genius in disguise.

The Discipline of Time Arbitrage. Time arbitrage is being willing to maintain a 3-5 year time horizon when most investors

and analysts are thinking about the next quarter. [This represents] a willingness to buy stocks that others are selling for short-term reasons. Many market participants want/need short-term results and so focus is on things like: Catalysts, short-term expectations, quarterly results …

Why Does This Work? Focusing on the long-term is difficult because:

- Takes patience — There can be periods of under performance.

- Most investors (clients) want results quarterly, or at least yearly, and so most money managers try to accommodate these short-term demands. (i.e. who cares what Apple looks like in 3 years, how many iphones are they going to sell this quarter??)

- Short-term thinking (among investors, fund managers, and corporate management teams) is pervasive now, and the speed of technology and information probably intensifies this view.

All of these decisions being made for short-term reasons creates opportunity (and the biggest market inefficiency in my opinion) for those who can look out 2-3 years. Source: Saber Capital Management

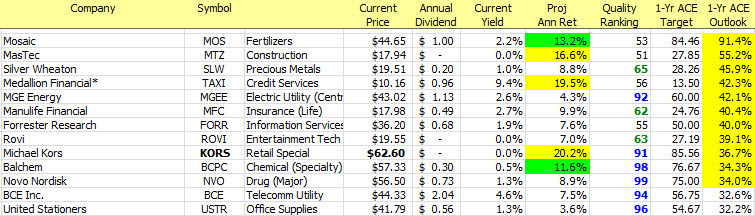

StockSearch Results: Hugh’s Hunt For 52 Week Lows. Hugh maintains a short list of vetted stocks, most of which he has been a long term shareholder. He monitors for accumulation opportunities when one of his favorites approaches a 52-week low. For the screening results shown, we’ve limited the field to high-quality (excellent) stocks that are within 5% of their 52-week low, while demanding above average financial strength. [Source: www.manifestinvesting.com StockSearch, 3/17/2017.]

The Long and Short of This Week’s Fave Five

The Long & Short. (March 17, 2017) Projected Annual Return (PAR): Long term return forecast based on fundamental analysis and five year time horizon. Quality Ranking: Percentile ranking of composite that includes financial strength, earnings stability and relative growth & profitability. VL Low Total Return (VLLTR): Low total return forecast based on 3-5 year price targets via Value Line Investment Survey. Morningstar P/FV: Ratio of current price to fundamentally-based fair value via www.morningstar.com S&P P/FV: Current price-to-fair value ratio via Standard & Poor’s. 1-Year ACE Outlook: Total return forecast based on analyst consensus estimates for 1-year target price combined with current yield. The data is ranked (descending order) based on this criterion. 1-Year S&P Outlook: 1-year total return forecast based on S&P 1-year price target. 1-Yr GS: 1-year total return forecast based on most recent price target issued by Goldman Sachs.

Fave Five Legacy (Tracking Portfolio)

The relative/excess return for the Fave Five tracking portfolio is +0.8% since inception. (The absolute rate of return is 19.0%.) 48.5% of selections have outperformed the Wilshire 5000 since original selection.

Tracking Dashboard: https://www.manifestinvesting.com/dashboards/public/fave-five