Photo: http://www.detroitmovestheworld.com

This Week at MANIFEST (11/17/2017)

“9. Don’t Rush. You don’t need to already know what you’re gonna do with the rest of your life. Don’t panic. You will soon be dead. Life will sometimes seem long and tough and, God, it’s tiring. You will sometimes be happy and sometimes sad, and then you’ll be old and then you’ll be dead. There is only one sensible thing to do with this empty existence, and that is fill it. Life is best filled by learning as much as you can about as much as you can, taking pride in whatever you’re doing, having compassion, sharing ideas, running, being enthusiastic, and then there’s love and travel and wine and sex and art and kids and giving and mountain-climbing. But you know all that stuff already. It’s an incredibly exciting thing, this one meaningless life of yours. Good luck and thank you for indulging me.” — Tim Minchin (Nine Life Lessons)

Let Me Save You Some Time

Those of you who catch some CNBC during the day probably recognize Josh Brown as one of the mainstays on the Halftime Report. From his books, Backstage Wall Street and the co-author stint via Clash of the Financial Pundits (with Jeff Macke) it’s clear that he and his colleagues see some of the same perspectives that we do. We’ve covered those complementary notions before here: Reformation: Center Stage.

It was refreshing spending a few moments in Detroit this past Thursday and Friday. That may seem strange to some of you but the city is truly engaged in a renaissance. The image above (and link provided) is part of Detroit’s compelling invitation to locate a second HQ here. I’m told that Detroit will likely make the “short list” as this continues to develop.

Detroit moves the world. We also know Detroit as the origins of the modern investment club movement — as championed by George Nicholson. As the first snow fell, it was refreshing to reflect on the dreams, aspirations and gifts bestowed by Nicholson and the community he nurtured. I took a moment to stop by the historic Rackham Building, the birthplace of the National Association of Investors (1951) and a movement that has favorably influenced the lives and investing experiences of so many of us. Nicholson was also a founding influence behind the Financial Analysts Society of Detroit and was a regular attendee … and routinely tendered the first question of the Q&A segment by asking the presenter to share their thoughts on “their greatest challenge.”

I assumed my seat at lunch on Friday next to a friend that I hadn’t met (yet). After brief introductions and observations about snow, I asked, “Did you know George Nicholson?” He smiled. “As a matter of fact, I spent last night with a couple of the Nicholson boys.” Wow. It turned out that his father had been influential in a few of Nicholson’s enterprises going back to the 1950s and 1960s and beyond. It’s a small world. It’s a Better World because of Nicholson’s contributions to the world of investing.

The theme of a better investing world resonates in Josh Brown’s perspective, too. Jason Raznick of Benzinga.com had arranged a town hall meeting format with Josh on Thursday night. If you’re not familiar with Benzinga, Jason has created a Bloomberg-like entity for investors and traders in Detroit that has become quite formidable. Thursday night turned out to actually be a better opportunity to compare notes and spend time with Josh as he shared observations about a number of things.

- Caveat emptor. He shared that (1) He’d been dismissed (sent home) not once, but twice from summer camp as a child. (2) He knows the Wolf of Wall Street and spent some time in similar trenches. (3) He’s been part of a couple of crash-and-burn initiatives.

- That last one is actually a virtuous attribute. He’s been there and done that. He considers his evolution from stockbroker to registered investment advisor to be among the best decisions of his life.

- Incentives Matter. Incentives, good and bad. They both affect performance and behavior in the markets. Incentives matter. Often they dictate the probability of potential outcomes in very foreseeable ways.

- Regulation FD Killed Most of the Rhinos Returns. So there. He said it. “Besides the growth in the number of funds, something else changed in the hedge fund space. Regulation Fair Disclosure (Reg FD) came into effect in 2000. This SEC-mandated rule forced all publicly traded companies to disclose material information to all investors at the same time. Prior to this, hedge funds had a huge advantage in terms of the information they could obtain prior to other investors. Reg FD changed that. This, combined with the large number of funds chasing similar securities and using similar strategies, has resulted in much lower performance for investors.” — Ben Carlson

Speaking of Ben Carlson, he attended the session on Friday. Hopefully we’ll get a chance to spend more time with Ben, too. Regular readers will recognize that his articles are frequently cited in our Results, Remarks & References section. Here’s a couple of Josh’s slides from Friday, including the famous (infamous?) CNBC Decabox:

Of Dragons and Debate: Active vs. Passive

“I’m so sick of the active vs. passive debate.” “The real debate is likely high cost vs. low cost … or faith-based versus systematic.” The librarians of the investing world are always stuffing things into boxes and categories. Some fodder for the dragons:

- “The S&P 500 Index Funds Are Not 100% Passive.” Ben Carlson has referred to the S&P 500 as the World’s Largest Momentum Strategy The S&P 500 is constantly re-balancing and the cap-weighting emphasizes Apple, Microsoft, FaceBook, Amazon and Johnson & Johnson. S&P 500 (VFINX) routinely has a 4-5% turnover as companies come and go. That’s not passive.

- (Mark here) I’d take it a step further and remind investors a la Ralph Acampora from a Detroit stage in 2001 that lost decades happen. That’s right. He told the audience to pick stocks or different funds, because the S&P 500 was about to get “killed.” Ralph was right.

- Sometimes a fund isn’t passive at all but is classified as a “passive ETF.” Josh cited a WisdomTree fund that is hedging European baskets vs. Japan and currencies in both directions for both geographies. “That may be 6-dimensional CandyLand, but it’s NOT passive.”

And finally, we know that some of our sleep-at-night active investing would be deemed quite “passive” but on closer examination, they’re NOT. Anything but. We buy. We hold … for as long as it makes sense to do so. In the case of our Bare Naked Million Portfolio there have been less than ten sell transactions since Christmas 2005. The turnover is less than these large “passive” index funds. And by the way, that bare naked $1,000,000 is now worth $3,177,277 (11/10/2017) — a “passive” annualized total return of 11.2% vs. 7.3% for the “actively” managed WIlshire 5000 (VTSMX) over the same time frame.

Thanks for the refreshing perspectives, Josh.

MANIFEST 40 Updates

Round Table Stocks

- Illumina (ILMN)

- ResMed (RMD)

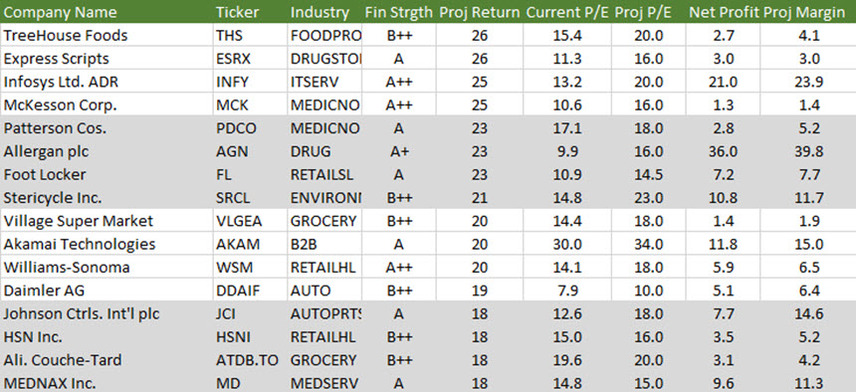

Best Small Companies (2018)

Round Table Sessions (Video Archives)

Results, Remarks & References