Merry Christmas! Bless Us, EVERYONE!

Holidays. We have much to be thankful for … notably the smiles on the faces of investors who have persisted through the Great Recession and experienced/realized fairly massive returns over the last few years. As we approach the end of our 10th year at Manifest Investing, all of us extend the warmest Seasons Greetings to all of you!

We’re already looking forward to celebrating our 10th birthday — and the launch of our 11th year — as Groundhog Day 2015 (2/2/2015) approaches. We’ll celebrate in a variety of ways, continuing to extoll the virtues of investment clubs and community-centered investing. The Round Tables will be part of that and we’re thankful for the contributions of Ken Kavula, Cy Lynch and Hugh McManus. We’re equally thankful for our guest damsels and knights: Kim Butcher, Herb Lemcool, Susan Maciolek, Anne Manning, Matt Spielman, Nick Stratigos … and last but certainly not least, our audiences who cast their votes monthly. You guys are the BEST.

We’re planning additional festivities which you’ll be hearing about soon. And you can listen for the sound of reindeer on your roof knowing that you’re in the hands of Kurt Kowitz, our technology manager. We’ve said it before, but without Kurt, the cost to deliver Manifest Investing to you would increase by at least one digit, maybe two. We’ll be unwrapping some cool gifts soon … and the prototype tinkering with the Equity Analysis Guides is likely the tip of a features iceberg. Thanks, Kurt!

For now, we nudge you as you unwrap this week’s batch … and we share a compendium of correspondence. You are not alone.

Merry Christmas, everyone!

A Bridge To Better Understanding

We’ve shared similar letters of consternation from investors in the past … and they come in many flavors. One of our all-time favorites was our visit to Narnia and our suggestion that The Couch Is Alright. Another memorable exchange came with “Nell” as we helped her to Make It Through The Night.

Where am I going wrong? I check out a stock, like it, and check it out on Manifest Stock Research. It looks good, you like it too. For confirmation I dig deeper — and [audit and verify assumptions using MyStudy]. Next thing I know, I feel like I get shot down when you show four or more reasons why the company is not worth an investment and say the quality is not to our standards. Is one screen looking at long term and the other at short term? Are you practicing April Fool tricks five months early?

We asked for an example. Chicago Bridge & Iron (CBI) was provided. CBI is actually a very compelling opportunity. There are some strong market drivers, long term. And the company is part of this week’s update batch — so let’s take a closer look.

I’m wondering where we differ. The PAR is 20-25% or so — making it somewhat speculative. The global recession has taken its toll with a fairly substantial price drop over the last several months. (From $89.20 down to $37.78 … -58%)

I don’t know but I wonder if investors and pundits are troubled over the Shaw acquisition?

Here’s a look at a Value Line data-based Equity Analysis Guide for CBI:

Be sure to account for the Shaw acquisition in your analysis. (This means you probably have to ignore anything before 2012 on a traditional SSG.) The step change in sales in 2012 was due to buying Shaw. When imagining what the future holds, be sure to emphasize the information that deals with the new, combined, company.

That could also lead to some significant differences between your study and the analyst consensus.

S&P has a fair value of $80.80 (recently adjusted downward from $87), so they think it’s significantly under priced at $41.

Thanks for the suggestion but, while I only mentioned one example when writing you, the same thing occurred over fifteen investigations. It leaves you with the feeling the entire market is overpriced so it might be better to hibernate until the pull back. I was particularly disturbed over CBI as they seemed a good candidate. Perhaps Lady Luck will lead me to a candidate where research and analysis will both agree. Thanks for your input.

Although luck is definitely involved in investing … we can look beyond Lady Luck a bit.

I think we’re seeing a symptom that’s related to the recent run in stock prices. This has been going on at the same time as an erosion of fundamentals. We’ve commented on this before — noting that in many cases, the only way to realize these return forecasts is if relatively high P/E ratios come home to roost.

I think CBI is a great candidate. The price has dropped enough to capture the attention of Hugh McManus. (grin)

Seriously, for a non-core stock (but one with relatively high quality) we need to demand a higher return forecast when considering purchase. We also must admit that a persistent or deepening recession will do things to CBI that are similar to 2008-2009. The stock price suggests, at least to me, that many people consider this to be a work already in progress.

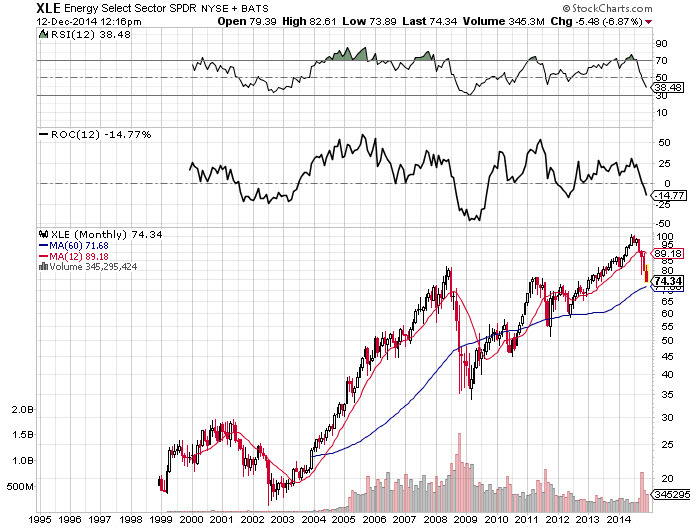

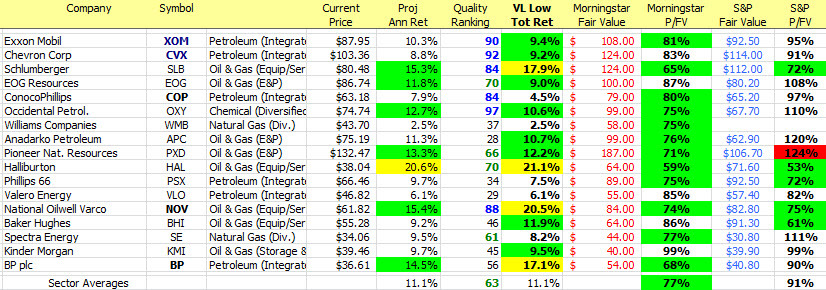

If they’re wrong, it’s a heckuva buying opportunity. And for a long term investor with a long term perspective, CBI is probably a lot like BP (BP), Schlumberger (SLB) and others in the oil patch these days. The next year or two could be rough and represent an opportunity for accumulation. But make sure the companies are built for survival if you decide to “go there.”

We feel your frustration but we still believe that a good StockSearch, directed at high-quality companies with elevated return forecasts can do a lot to populate the area underneath just about any investing Christmas tree.

Coming Events and Attractions

Our expanded coverage of the update stocks this month continues as part of our quarter long test drive of this feature and the studies and shared ideas it delivers. Please tell us what you think and feel free to join in the Forum discussions for the deeper dives on some of the stocks.

Save the Date: The December Round Table will be held on December 30 at 8:30 PM ET. Register via: https://www2.gotomeeting.com/register/256833802

Round Table Tracking Portfolio

Stocks Likely To Be Covered:

- Chicago Bridge & Iron (CBI)

- Copa Holdings (CPA)

- Qualcomm (QCOM)

Companies of Interest: Value Line

The average Value Line low total return forecast for the companies in this week’s update batch is 4.7%.

The number of companies with slightly reduced fundamentals combines with the price increases over the past month to produce some fairly low return forecasts.

Trex (TREX) has been a personal favorite since my Better Investing days … and it leads a lonely group of companies with bolstered fundamentals. As a reminder, we monitor changes in the long term forecasts by Value Line and share those that have been adjusted 20-25% or more (up or down) as “Materially Stronger” (Up) or “Materially Weaker” (Down). We consider this a best practice and a nudge for stock watchers or shareholders to update/audit existing analyses. In some cases, it may trigger a study of opportunity.

Materially Stronger: Trex (TREX)

Materially Weaker: Owens Corning (OC), Layne Christensen (LAYN), Tile Shop Holdings (TTS), Enernoc (ENOC), Rayonier (RYN)

Standard Coverage Initiated:

Discontinued: Kimball (KBALB), Foster Wheeler (FWLT), TIBCO Software (TIBX), Concur Technologies (CNQR), Conversant (CNVR), Compuware (CPWR), URS (URS)

Companies of Interest: Morningstar

The average price-to-fair value (P/FV) ratio at Morningstar for the companies in this week’s update batch is 106%.

Companies of Interest: S&P

The average price-to-fair value for the companies in this week’s update batch is 105% — according to S&P.

Market Barometers

The median Value Line Low Total Return (VLLTR) Forecast is at 3.4%, plummeting from 4.2% last week as the Thanksgiving Swoon gives way to a Christmas Rush of multiple 1-2% daily gains in the overall market.

Stocks to Study

The following update stocks are ranked in the top 10th percentile of all companies we follow (MANIFEST Rank > 90):

Manifest Investing is a subscription site (ONLY $79/year for individual investors). Contact us (via manifest@manifestinvesting.com) if you would like to explore our resources as an investment club. We offer group discounts to clubs. Discover and explore our research on stocks and funds, our seminars and tools for portfolio design & management. Experience the demonstrations of a 7-decade old time-honored philosophy and method that has supported legions of long-term investors. Go to http://www.manifestinvesting.com and create a trial account today. Send us an email if you’d like to access a FREE fully-functional test drive through 2/28/2015 without providing a credit card. Merry Christmas!

3M announces $12B buyback.

3M announces $12B buyback.