“I would like to see AFLAC under your scope.” — Jack Ellison

Thanks, Jack. For those who don’t know Mr. Ellison — he’s one of the leaders of the award-winning GaAs investment club near Sacramento, California. Gallium Arsenide (GaAs) is a compound of the elements gallium and arsenic and the chemical is used in the production of semiconductor devices. The connection to and inspiration from Silicon Valley is pretty clear.

The GaAs investment club was the leading group in the Value Line/NAIC club portfolio contest back in 2001 and was honored at the 50th anniversary national convention in Detroit.

AFLAC Duck: Uhhhh … he said arsenic. I really wish he’d not do that.

MI: No worries. Besides, we thought the only thing you ever said is “AFLAC!”

AFLAC Duck: That’s my stage persona.

MI: We hope the healing process is going well and sorry to hear of your set back.

AFLAC Duck: Thanks. I needed some rest. Since I stopped that whole migration thing … it’s way, way over-rated, by the way … I’ve gotten a little pudgy. A little time here with the workout equipment in Physical Therapy is probably just what the doctor ordered. Hollywood can wait.

MI: You’re not concerned that a gecko or some furry critter will steal your spot?

AFLAC Duck: Always a concern. Who are we kidding? Wally Pipp thought it’d be OK to take a day off. If you see any critters around the offices in Columbus that remind you of Gehrig, let me know.

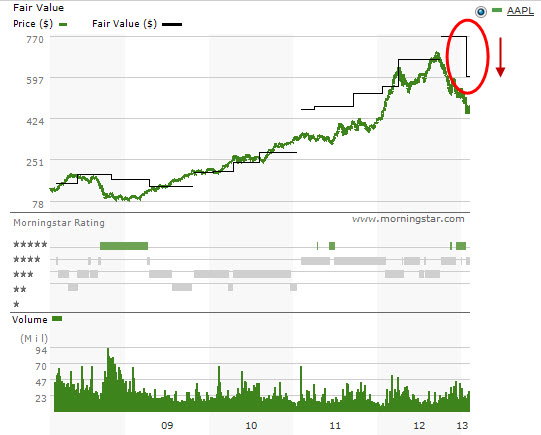

MI: Consider it done. And now for a closer look at a community favorite and paragon of stability over the decades. But at the same time, we could make a case for a couple of really big speed bumps over the last few years — and some turbulent challenges that we’d consider more temporary than terminal.

AFLAC Duck: Terminal is not such a good word either around here.

MI: Sorry. Get well soon.

Aflac, Inc. provides supplemental life and health insurance services. The company is a general business holding company and acts as a management company, overseeing the operations of its subsidiaries by providing management services and making capital available. Its principal business is supplemental health and life insurance, which is marketed and administered through its subsidiary, American Family Life Assurance of Columbus, which operates in the United States and as a branch in Japan. The company operates business through two segments Aflac Japan and Aflac U.S. The Aflac Japan segment provides child endowment and ways products and operates as a branch of Aflac and principal contributor to consolidated earnings of Aflac. The Aflac U.S. segment sells voluntary supplemental insurance products including, loss-of-income products and products designed to protect individuals from depletion of assets. AFLAC was founded by John Amos, Paul Amos and William Amos on November 17, 1955 and is headquartered in Columbus, GA. [Wall Street Journal]

Business Model Analysis

The top-line for financial sector companies like AFLAC is book value (BV). The bottom line is EPS, as always — and the relationship (difference) between the top-line and bottom-line for financial sector companies is return-on-equity (ROE) and we pay close attention to the profitability trend on display for ROE.

Projected Average P/E

The forecast for a future P/E ratio for AFLAC is little different from the rest of the banking and/or insurance industry. Will ROE return to historical levels or “labor” in the New Normal? As an investor in financial sector enterprises, this is a key assumption or judgment.

In the case of AFLAC, we’d probably argue for stabilization and statistically a median of 10x (plus or minus 2x) seems to be reasonable.

Equity Analysis Guide

Using the 11% book value growth rate, a ROE forecast of 13% and a projected average P/E of 10x — the projected annual return is 11.6%.

This compares to a Value Line low total return forecast of 11.5%.

With the median return (all stocks) at 7.1%, the 11.6% return forecast is fairly compelling — particularly when considering the 99th percentile quality ranking for AFLAC (AFL).