Happy Birthday, bivio!

Expected Returns Cover Story … first posted on September 1st, 2009. We revisit this feature today as we celebrate bivio’s 15th birthday and honor their service to legions of investment clubs and individual investors with the best service and most cost-effective record keeping software and support network for investment partnerships. We’ve known you since day one. You’re simply the best!

In his own words, Nicholson talked of investment clubs as his “Grand Experiment.” Their purpose? Education. Period.

The talking heads are obsessing over Septembers nearly ten years ago or one year ago when massive upheaval in the financial markets was ramping up. In the end, the demise of household names like Lehman, Bear Stearns and Merrill Lynch would go on to prove that this was no ‘speed bump’ in history. My thoughts drift to other foundations as autumn approaches, to nearly 70 years ago when a small group of young men wandered into the office of a professional investor in Detroit. “We want to learn how to invest.” “OK, but we’re gonna have some rules of engagement: we’ll operate professionally in a business-like manner, we’ll invest regularly and we’ll stay invested as long as it makes sense to do so in leadership growth companies …”

bivio: “where two roads meet” We first met the key players at MANIFEST business partner, bivio, over ten years ago. Their mission then and their mission now is to create an environment of success for groups of investors. As their tenth birthday approaches, we look forward to what the future holds for investors.

bivio: “where two roads meet” We first met the key players at MANIFEST business partner, bivio, over ten years ago. Their mission then and their mission now is to create an environment of success for groups of investors. As their tenth birthday approaches, we look forward to what the future holds for investors.

bivio is a web-delivered application, enabling groups of individual investors to create and manage their own investment clubs – it’s like creating your own personal mutual fund. By making the administrative tasks easier, bivio has succeeded in widening the learning window. We look forward to working with them, building on that foundation and resources.

All the things I remember, Summers never looked the same …

Years go by and time just seems to fly, but the memories remain.

In the middle of September, We still play out in the rain. — Daughtry.

That autumn day in 1941 in Detroit was a critical moment in the modern investment club moment. The professional investor was George Nicholson, Jr. CFA and the principals went on to form the National Association of Investors ten years later. Some of you may wonder why our attention focuses so much on investment clubs. We clearly appreciate that some of you are not clubbers. That said, the vast majority of our subscribers are either active or have been active in an investing partnership.

Shortly after joining the Better Investing staff as senior contributing editor back in 1997, I worked with the Motley Fool founders on an article that proclaimed that fool.com was the world’s largest investment club. My Foolish friends were wrong. I followed shortly thereafter with an article that hailed technological advances and declared that the umbrella organization had become one big investment club. I, too, was wrong.

The heart and spirit are in the right place … and the power of Community is incredibly important. Look no further than our discussion of the “Wisdom of Communities” (Expected Returns, June 2008) or our back-to-school features and tributes to tradition like Muskrat Pageantry (ER, March 2008.)

In his own words, Nicholson talked of investment clubs as his “Grand Experiment.” Their purpose? Education. Period.

Building Better Futures

Let me be clear. We know that people engage learning opportunities in a variety of ways. Whether from reading books, attending classes, poking around online, observing best practices from successful individuals … it’s a long list. The genesis of investment clubs was clearly centered on a learn-by-doing experience by leaning on friends.

And that’s what wrong with the previous articles. Our family attends a church where 28,000 people can show up for worship on Christmas and Easter. I can’t imagine learning-by-doing with a group that large. Hence, we form small groups where “we” comes to life. Clubs (We) cultivate patience and discipline while seeking the opportunities achieved by incrementally better returns. It’s quite literally the stuff that dreams are made of.

The Genesis of Clubs

Nicholson shared in later years that the motivation for Fred Russell and the other young men was quite literally, freedom. Russell dreamed of the day when he could walk away from his day job to operate his own business. This ultimately became reality as he went on to a Howard Johnson franchise in years ahead.

Here is the core of the modern investment club movement:

1. Provide a way for many people to start an investment program in a small way, without too much experience, and build their investment knowledge to the point where they have the ability to acquire a sizable investment portfolio and manage it profitably.

2. Broaden the awareness and interest of individuals in the ownership of equities … in many cases, this takes shape as members/practitioners have as great an interest in helping others to learn about [effective] investing.

Most clubs form as a general partnership and suggest that their partners invest relatively small amounts ($20-50, usually) on a monthly basis into the club portfolio. In fact, if you’re visiting and considering joining a club and the figure is much higher than that — caveat emptor. It’s not about the total assets, it’s always been about growing the unit value at superior rate.

In the early days of investment clubs, think about the environment. The participants were still using slide rules and doing multiplication and division by hand. (Gasp) It was difficult to buy stocks in “odd lots” and commissions were substantial on these 100-share increments.

One of the earliest drivers was the pooling of the finances, enabling a lower cost ratio than individuals could achieve on their own. The intent was to spread out expenses.

But the “pooling” didn’t stop there. Think about access to information. Company reports were hard to obtain and clubs divided up the odyssey and the analysis for survival.

The Mutual Club of Detroit provides one of the standards of excellence. One member has donated $20/month since February 1948 building an account that reached seven digits (despite a fair number of significant withdrawals to fund life experiences) and a rate of return of approximately 13% since inception.

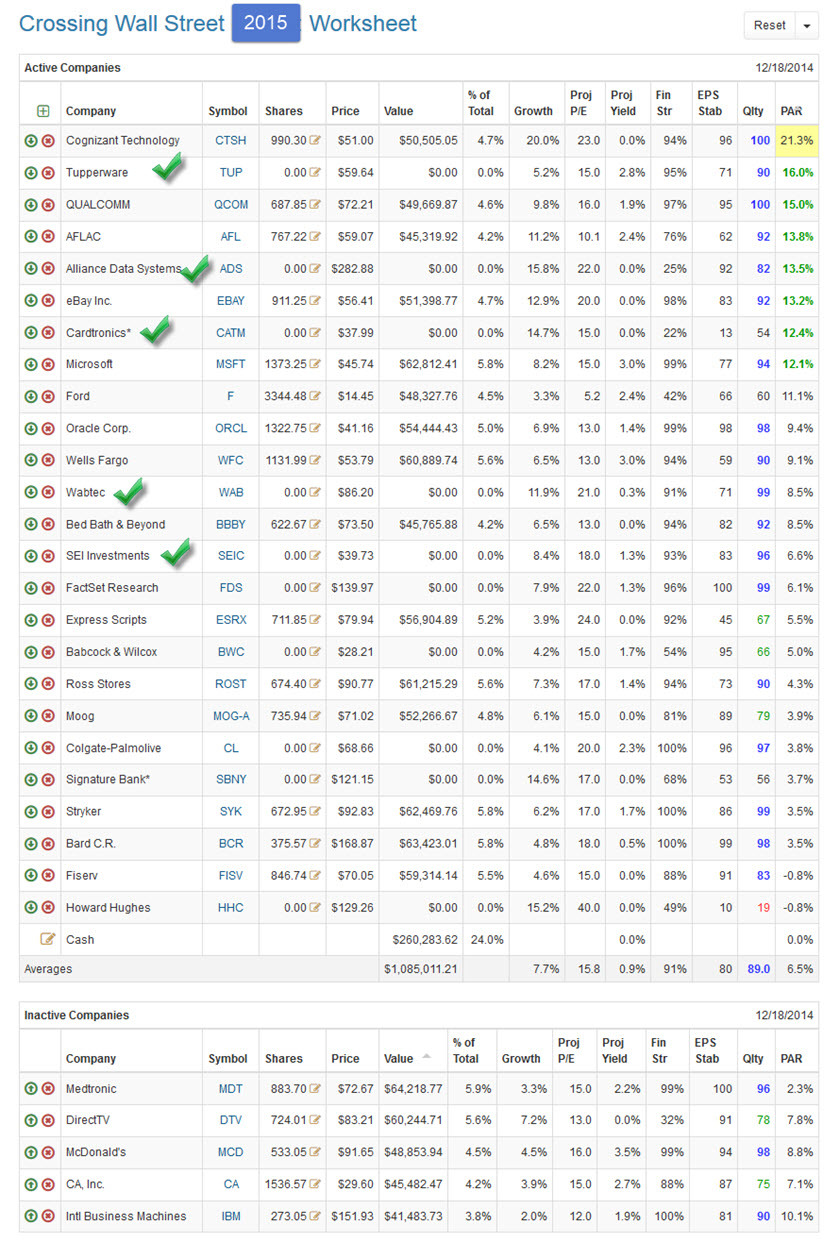

Model Behavior. Demonstration investment clubs, like the Brighton (Michigan) group meet monthly to explore and learn together. The club dashboard is one of the published portfolios available at MANIFEST. The club is education-centered and led by a group of volunteers from the southeastern Michigan region.

Model Behavior. Demonstration investment clubs, like the Brighton (Michigan) group meet monthly to explore and learn together. The club dashboard is one of the published portfolios available at MANIFEST. The club is education-centered and led by a group of volunteers from the southeastern Michigan region.

Fast forward to today. Transaction costs have plummeted and access to investment information has literally exploded. A couple of the original drivers of the “Grand Experiment” have changed pretty dramatically.

At The Crossroads

What hasn’t changed is (1) the business-like approach and (2) the incredible learning power of collaboration within the Community.

Enter bivio. One of the treasures delivered is effective accounting support. Keeping the club and individual records and generating a tax return with a couple clicks means that a very special resource is redistributed to club partners … TIME.

With administrative tasks reduced to background music, time is liberated to explore and seek better investing opportunities. The record-keeping is still crucial but the emphasis shifts to learning-by-doing, together with friends. Investing better.

And dancing in the September rain, with our friends, is what our investing journey is really all about.

At bivio, “Bags Fly Free” there are no hidden annual charges to file annual tax reporting. Explore the resources at bivio.com and experience investing with some new friends.