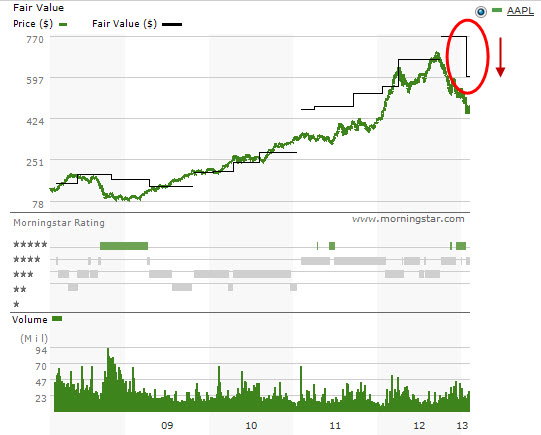

FYI … both Morningstar (from $770 to $600) and S&P have reduced their fair value estimates on Apple (AAPL) in recent days. Analyst consensus estimates for sales and EPS for years ending 9/30/2013 and 9/30/2014 also reduced. The impact on our return forecast will take it from 24% to 18-19% — still undervalued, just not as much. Point-and-figure (PnF) sentiment on www.stockcharts.com has turned “Prelim Bullish”.

I’d like to see confirmation on the P&F chart over the next few sessions before I get positive about Apple. That and I’d like to see the hedge fund extortionist behavior be recognized for what it is and with unrestrained brutality, eliminated so Apple can go back to making the next great device and continue to build value in the company. I’ve never seen a shareholder lawsuit do anything but drain resources from a company for the sole benefit of lawyers at the employees and shareholders expense.

Ditto on the confirmation, there’s still considerable institutional downside pressure “out there.” I’m not sure that the hedge thing is that big of a deal and yes, delivered innovation is an Apple hallmark. As they say, on with the show. Barry Ritholtz sings in harmony with you here: http://www.ritholtz.com/blog/2013/02/the-collossal-gall-of-bad-apple-investors/