Is Stericycle a Sell?

Stericycle (SRCL) was added to the Round Table tracking portfolio back in February 2014 at a stock price of $114.00. It has since lagged the market by some -21.5% (annualized) leaving some to wonder if it isn’t a sell candidate despite trading near 52-week lows.

The Value Line perspective — in a nutshell:

Our near-term investment outlook has grown more pessimistic over the past three months. Specifically, Stericycle is now ranked to under perform the broader market averages over the coming six to 12 months. The issue does hold wide recovery potential, assuming our long-term projections aren’t far off the mark. (Matthew E. Spencer, CFA August 25, 2017)

Perhaps, but trading near the 52-week low delivers a 1-year zoning position of 3.7% with a 1-year target price of $107. The “average stock” has a 1-year zoning position of approximately 80%.

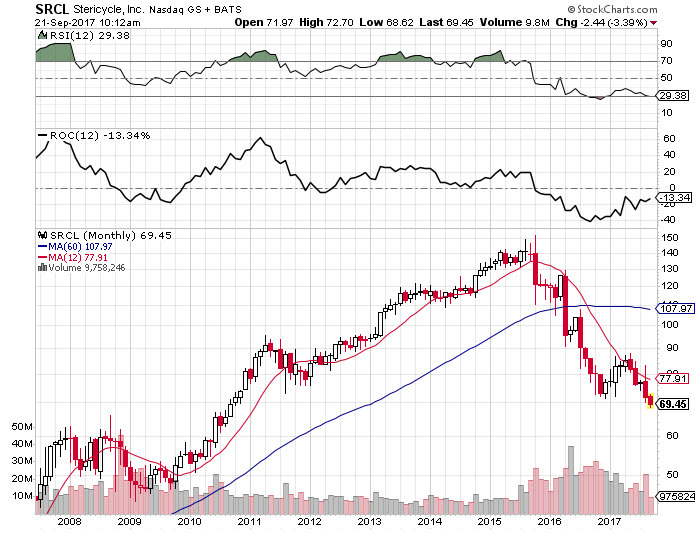

As shown in the accompanying chart, SRCL is now “oversold” (RSI<30).

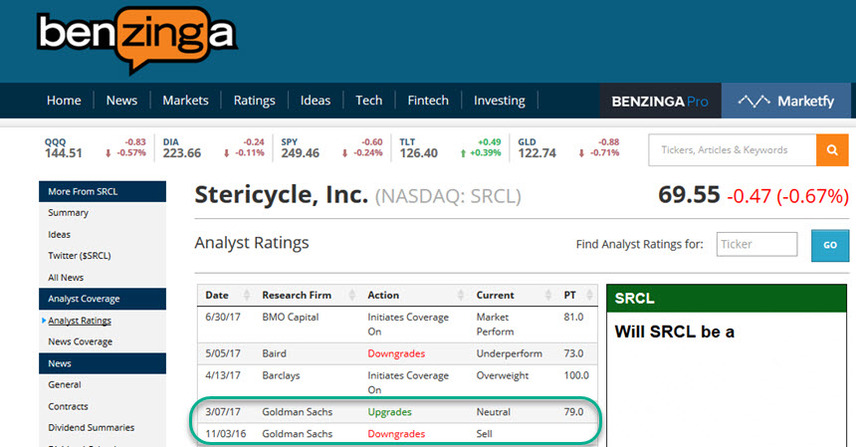

Goldman Sachs has not changed their outlook from March — at least not in a public release or not yet.

This overview does display a spectrum of expectations for the 1-year target range.

Morningstar continues to maintain a fair value of $110.

This delivers a price-to-fair value of 70/110 = 63.6%

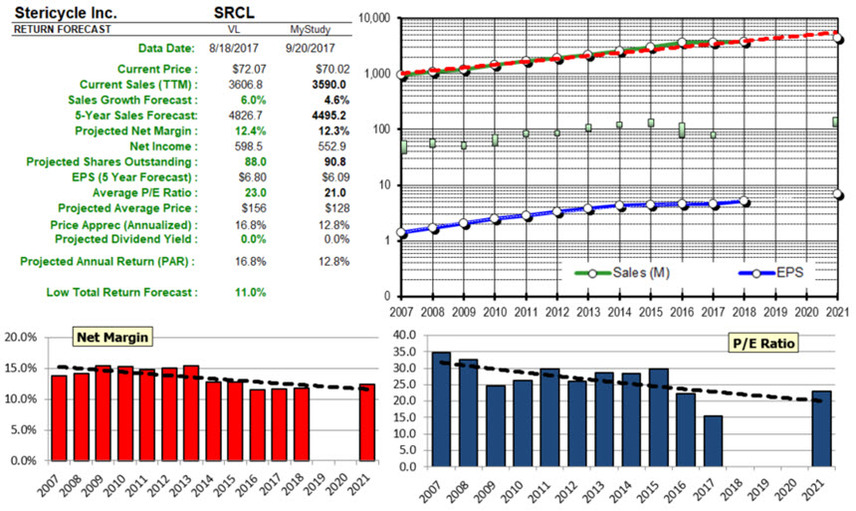

Growth: “These assumptions allow Stericycle to approach $4.5 billion in revenues by 2021, reflecting a five-year organic revenue CAGR of 3.7%.”

We expect the near term may yet be volatile as Stericycle continues to manage headwinds in its core business, integrate Shred-It, design and implement an enterprise wide information technology system, and ultimately restore confidence in a business that we continue to believe has the building blocks in place to produce reliable recurring revenue streams over the long run. (Barbara Noverini, August 10, 2017)

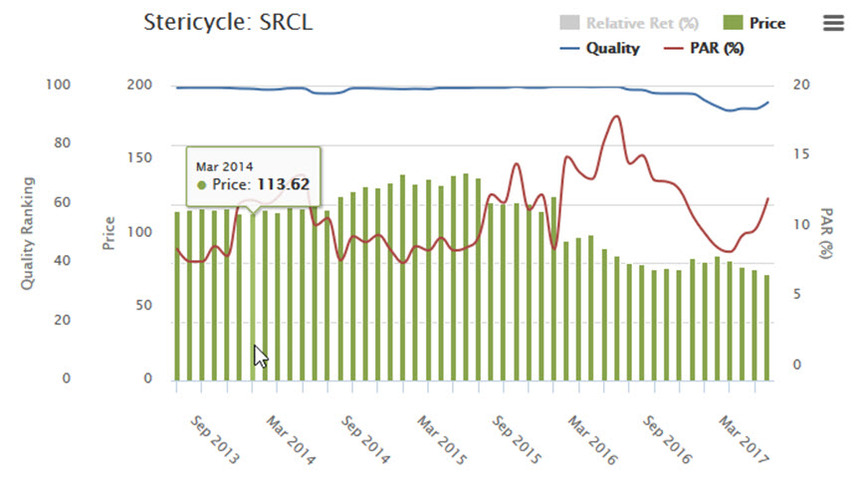

Did we miss a “trough” in PAR — a potential selling opportunity when the stock price hit $151.6 during 2015?

How about quality degradation?

As the accompanying chronicle shows, the PAR did not reach “auto-sell” levels during 2015 — but this image does rekindle those questions about the notion of “support and resistance levels” on PAR charts also. For some stocks, should we be setting low-PAR and high-PAR triggers much like Bollinger bands in technical analysis? I don’t know. But it’s worth some considerations and a pile of case studies, I’d think.